The global financial landscape is undergoing a profound transformation. As of 2026, the Islamic finance market is projected to reach a value of $10 Billion, driven by an increasing demand for ethical, asset-backed, and transparent financial solutions across the Middle East and Africa. However, as institutions rush to capture this growth, a dangerous misconception has taken root: the belief that “interest-free” is synonymous with “Sharia-compliant.” For banking executives, regulators, and Sharia scholars, this distinction between interest-free vs sharia-compliant banking is not merely semantic. It is the difference between an ethical facade and a robust, compliant financial system.

The Semantic Trap: Interest-free vs sharia-compliant banking

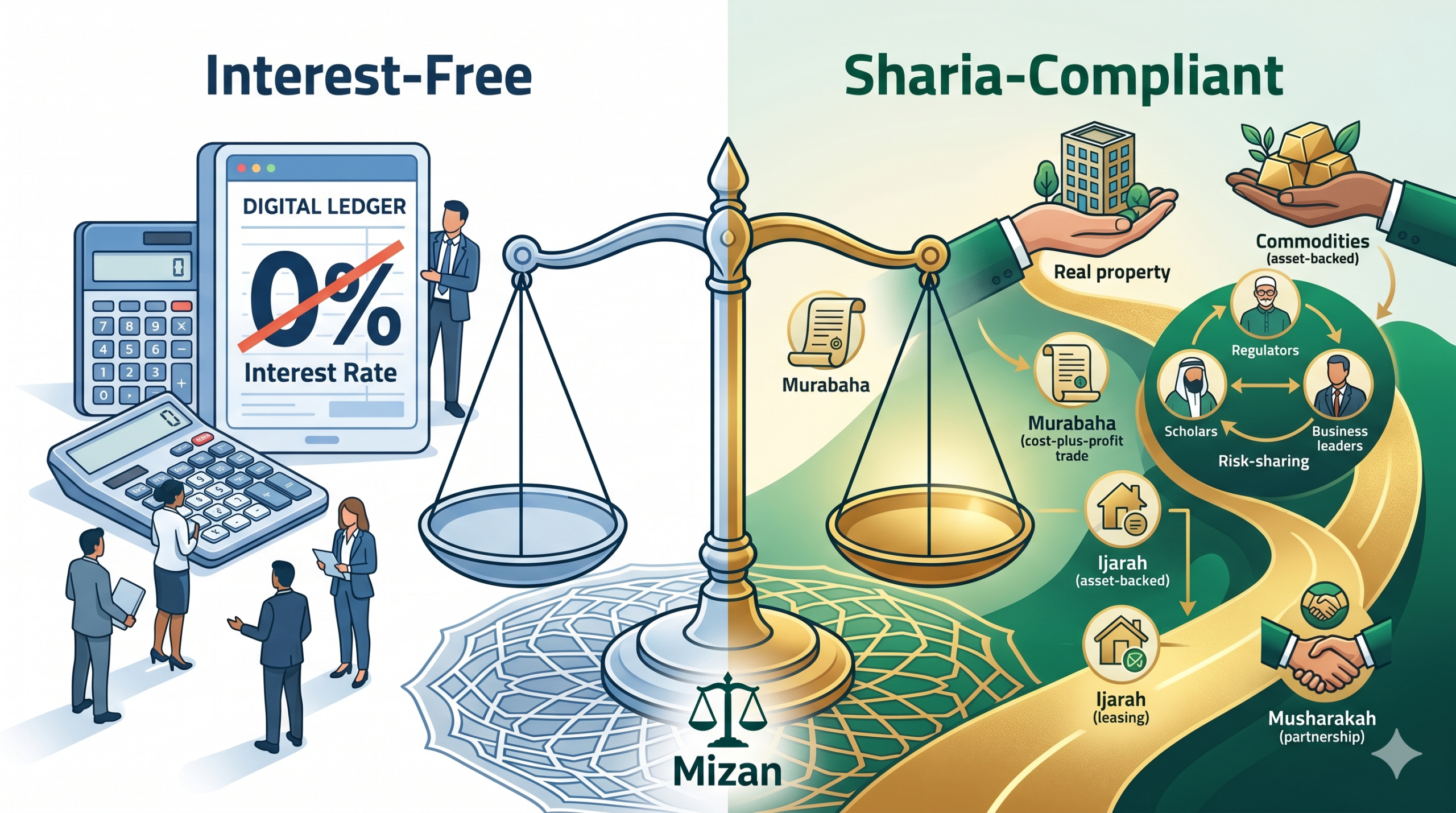

To the casual observer, removing the interest rate (Riba) from a loan seems sufficient. However, “interest-free” is simply a mathematical state; it describes the absence of a charge. In contrast, Sharia-compliant banking is a holistic economic model designed to foster equity, fairness, and risk-sharing.

In Islamic banking, the greatest risk is not always what appears on the product brochure. It is what happens inside the core.

A product may be described as non-interest. A financing plan may be introduced with Islamic terminology. But if the system still permits interest-based calculations, weak asset validation, improper transaction sequencing, or manual spreadsheet workarounds for profit allocation, then the institution is still exposed.

This is where the difference between interest-free and truly Sharia-compliant banking becomes very clear.

A bank may intend to operate correctly, but intention alone is not enough. If the platform does not enforce the right structure, compliance becomes fragile. It depends too much on human intervention, manual review, and after-the-fact correction. That increases operational risk, audit exposure, and reputational vulnerability.

We do not believe Islamic banking should depend on patches, workarounds, or good luck.

According to the Accounting and Auditing Organization for Islamic Financial Institutions (AAOIFI), true compliance requires that every financial product be linked to a tangible asset or a productive economic activity. While a conventional bank can offer an “interest-free” loan, it often lacks the underlying physical asset or trading transaction that is the hallmark of Sharia integrity.

This is the fundamental gap Mizan was designed to bridge. We built Mizan as a modern Islamic core banking solution that moves beyond simple interest avoidance to ensure complete contractual and ethical finality.

Why Conventional Cores Fail Islamic Institutions

Many institutions attempt to customize conventional core banking platforms to serve Islamic windows. This approach often leads to significant operational and regulatory risks:

- Rigidity of Legacy Systems: Traditional cores are often siloed and not adaptable to the real-time needs of Islamic finance.

- The “Form vs. Substance” Conflict: Conventional systems are built on IFRS standards that prioritize economic substance over legal form. Sharia-compliant finance, however, requires both form and substance to be aligned through specific contracts like Murabaha, Ijarah, or Musharakah.

- Manual Workarounds: When a system cannot natively handle Islamic workflows, staff are forced into manual reconciliations, increasing the risk of compliance errors.

We recognized these pain points — the burden of managing outdated, rigid IT systems and the high cost of vendor lock-ins. This is why we built Mizan from the ground up as an Afro-optimized, API-first platform tailored to the realities of emerging markets.

What Mizan Offers: Beyond the 0% Rate

Mizan is the first modern, African-built core banking solution designed to meet the unique challenges of financial institutions in emerging markets. It provides a streamlined, cost-optimized package that allows institutions to go live faster and at a lower cost than global legacy providers.

1. Built-in Sharia Workflows

Mizan does not treat Islamic finance as an add-on. We offer a platform where Sharia-compliant operations are automated, safeguarding the institution’s integrity and reducing the dependency on manual engineering for core changes.

2. Regulatory and Board-Level Assurance

One of the greatest fears for a Chief Risk Officer (CRO) is regulatory misalignment. Mizan offers:

- Pre-built Templates: Reporting modules aligned specifically to local requirements to reduce preparation time.

- Audit Trails: Cleaner reconciliation and visibility into deposits, loans, and liquidity for better supervisory confidence.

- Reduced Fine Risk: Minimized risk of regulatory fines through automated verification flows.

3. High-Velocity Innovation

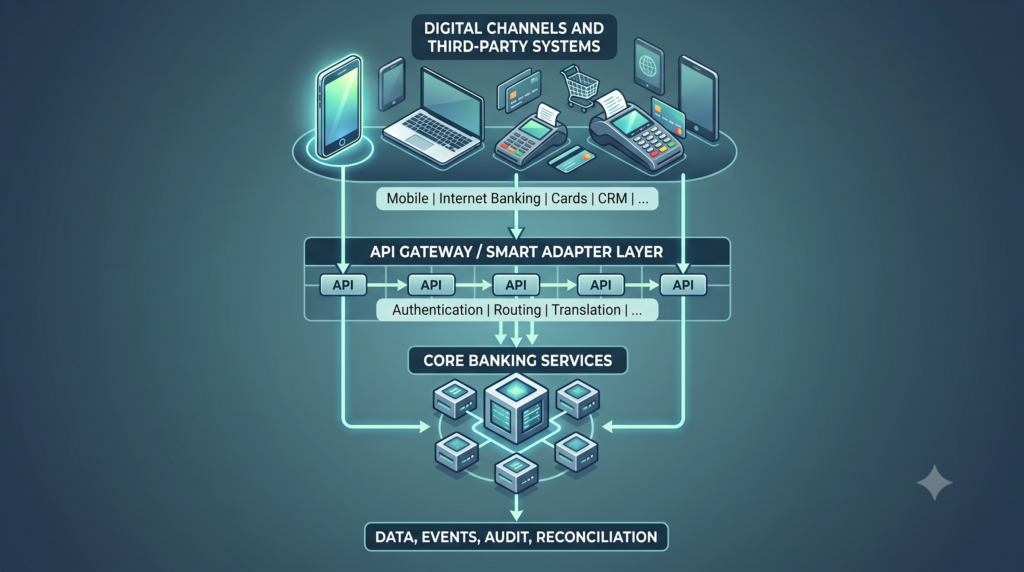

For the Chief Information Officer (CIO), Mizan provides an API-first modern core that enables:

- Seamless Integration: Integration with mobile apps, USSD, and fintech APIs for a faster channel rollout.

- Cloud-Native Flexibility: Delivered as a fully managed SaaS offering with local data residency, freeing you from foreign tech dependence and high FX costs.

- Rapid Product Launch: The ability to launch products faster to capture SME and youth markets.

4. Technical Superiority and Local Support

In the MENA and African regions, time-zone delays and foreign vendor dependencies can lead to crippling downtime. Mizan addresses this through a localized support model:

- 1-Hour Response Times: We provide immediate access to experts who understand local network issues and integration rails.

- Real-Time Troubleshooting: No more waiting for overseas support; our team provides real-time resolution to ensure operational confidence.

Leading the Next Frontier

The future of finance in emerging markets is not just “interest-free”; it is authentically Sharia-compliant. As major trends in the 2026 forecast period point toward the expansion of Sharia-compliant digital banking platforms and asset-backed financing, the choice of infrastructure becomes a choice of survival.

Mizan is designed for the bold leaders who want to transform their institutions for long-term profitability and shareholder confidence. We provide the competitive edge to be truly peerless in a market that demands nothing less than absolute integrity.

Is your institution ready to move beyond the facade of “interest-free” and embrace the power of true Sharia compliance? Discover how Mizan can empower your growth today.