Banks often mistake basic automation for artificial intelligence. Many roll out a script-based chatbot, place it in the mobile app, attach the word “AI” to their announcement, and expect a positive change in customer satisfaction. Yet the metrics barely move. Queries stay unresolved. Call center queues stay long. And customers revert to physical branches when digital channels waste their time.

The problem is simple. Script-based chatbots do not think. They do not learn. They do not anticipate needs or guide decisions. The chatbots also only follow rules that product teams write manually. This limitation is what fuels frustration, and it is why leading African institutions are shifting to deeper layers of intelligence.

True AI does not just answer pre-set questions; it predicts financial needs and manages wealth proactively. The banks that understand this shift will outperform those still relying on old ideas of what AI in banking should be.

Artificial intelligence in 2025 is changing every layer of banking. Across Africa and other emerging markets, institutions are moving from surface-level digital improvements to deeper intelligence built on predictive models, generative reasoning, and real-time data. This change is driven by rising customer expectations, constant fraud pressure, and the need to operate with leaner teams.

The next decade in banking will be shaped by systems that think, not systems that wait for customer input. To reach this level, institutions must understand what separates simple automation from true intelligence and how to architect for both prediction and advanced user experience.

This article explores what this new phase of AI in banking looks like, how it is reshaping customer experience, and why financial institutions across Africa and other emerging markets are accelerating their AI investments.

The Difference Between Automation and Artificial Intelligence

Many banks still treat automation as the final stage of digital transformation. Automation improves speed and consistency, but it lacks awareness. It only acts when a user triggers a process or when a staff member pushes a workflow forward. This limitation becomes clear when customers ask questions that fall outside predefined paths, and the system responds with generic or irrelevant messages.

Artificial intelligence addresses this gap. AI models learn from patterns across millions of data points. They adjust based on behaviour, not rules. AI models also analyse context and detect meaning in natural language. And they support decision-making for teams, not just customers.

To clarify the distinction, consider these differences across three layers:

1. User Interaction Layer

- Automation: Follows predefined scripts.

- AI: Understands natural language and context.

For example, a script-based chatbot can check a balance when asked. A true AI assistant can recognise that the customer checks the balance to confirm a deduction, then offer context about recent transactions or an upcoming loan repayment.

2. Decision Layer

- Automation: Executes fixed workflows.

- AI: Makes recommendations and learns from new information.

A rules-based engine can approve a loan if a customer meets fixed criteria. AI assesses risk dynamically based on behaviour, not just demographics or static credit files.

3. Analytical Layer

- Automation: Processes structured inputs.

- AI: Interprets both structured and unstructured data.

This includes analysing call transcripts, transaction patterns, credit behaviour, and customer interactions across channels. AI systems extract meaning where automation sees only inputs.

Understanding this difference helps leadership teams plan the right architecture. Institutions that only automate limit their competitiveness. Institutions that pursue intelligence build the foundation for predictive models, conversational banking trends, and advanced digital banking user experience.

Predictive Banking: How AI Stops Problems Before They Happen

Predictive intelligence is reshaping banking in emerging markets, especially in regions such as Nigeria, Kenya, Ghana, and Egypt. The next phase of AI in banking focuses on anticipating events rather than reacting to them. Institutions gain the ability to spot fraud, foresee customer distress, identify churn patterns, and recommend financial products at the right time.

Predictive banking works because modern AI systems consume and process large streams of real-time activity. They observe changes in customer behaviour that humans either overlook or recognise too late.

Below are core use cases where prediction is driving value.

1. Early Identification of Loan Risk

Traditional credit scoring models depend on static data such as income, account balance, or past repayment history. Predictive models evaluate dynamic behaviour, including:

- Transaction velocity

- Sudden spending spikes

- Declining deposit frequency

- Location and device indicators

- Peer group repayment patterns

This approach supports more accurate lending decisions, especially in African markets where formal credit history is often limited. As a result, predictive banking in Nigeria and other markets is gaining mainstream adoption.

2. Proactive Credit Risk Management

Non-Performing Loans (NPLs) destroy bank value. Traditional credit monitoring relies on lagging indicators, such as missed payments. By the time a payment is missed, the risk has already materialized, and recovery becomes difficult and expensive.

Predictive AI analyzes leading indicators. It detects subtle changes in borrower behavior months before a default occurs. These signals might include:

- A gradual decrease in average daily balance.

- An increase in gambling or high-risk transactions.

- A delay in payroll deposits for SME clients.

- Changes in spending velocity relative to income.

When the system detects these patterns, it triggers an early intervention. The bank can offer loan restructuring or financial advice to the customer before the default happens. This preserves the relationship and protects the bank’s capital.

3. Fraud Detection Before Loss Occurs

Fraud actors adjust their tactics constantly. Rule-based systems only catch what has happened before. Predictive models identify anomalies by comparing real-time activity against millions of historical patterns.

Signals include:

- Device fingerprint mismatches

- Suspicious IP locations

- Behaviour inconsistent with past habits

- Repeated micro-debits

- Multiple failed login attempts

This improves fraud prevention without increasing false alerts that frustrate customers.

4. Retention and Churn Reduction

Predictive AI can detect signals of customer dissatisfaction such as:

- Reduced engagement with digital channels

- Declining transaction frequency

- Negative sentiment in support conversations

- Irregular savings patterns

These insights allow banks to intervene with personalised offers or support.

5. Proactive Wealth and Savings Guidance

AI systems can forecast cash flow and recommend:

- Best times to save

- Expense patterns that might create risk

- Upcoming commitments

- Opportunities to move surplus funds into investment products

This moves banking from reactive support to proactive financial guidance.

6. Preventing Liquidity Crunches

Liquidity management remains a primary challenge for treasurers in volatile markets. Traditional reporting looks at yesterday’s closing balance to estimate today’s needs. This rearview approach exposes the bank to risk during sudden market shifts or currency fluctuations.

AI models analyze years of transaction data, seasonal trends, macroeconomic indicators, and even social sentiment to forecast liquidity requirements with high precision. A predictive model might identify that cash withdrawals spike in specific branches three days before a major religious holiday or during specific market events. It alerts the treasury team to adjust cash logistics proactively. This prevents service disruptions and optimizes the cost of cash.

Predictive intelligence is not a front-end feature. It requires a strong core that supports real-time streaming, continuous data quality, and open integration pathways. Banks that adopt predictive models without fixing foundational data architecture face accuracy challenges.

7. Predicting Infrastructure Failure

For the CTO, uptime is the ultimate metric. Legacy core banking systems are prone to unexpected outages, often caused by database locks or resource exhaustion during peak times. Predictive banking also applies to IT operations (AIOps).

AI agents monitor server logs, API latency, and database performance in real-time. They identify anomalies that precede a crash, such as a slow memory leak or a micro-spike in CPU usage. The system can then route traffic to healthy nodes or restart services automatically during low-volume windows. The result is a self-healing banking infrastructure that maintains 99.999% uptime, protecting the bank’s reputation during critical high-volume periods like Black Friday or salary week.

Generative AI vs. Scripted Responses: The Experience Gap

The gap between scripted responses and generative AI is wide. Scripted chatbots depend on predefined commands. They often fail when customers ask questions outside expected patterns. This breaks the user journey and forces customers to call support or visit a branch, which undermines the investment in digital transformation.

Generative AI changes this dynamic. It understands intent rather than keywords. It interprets complex queries and provides explanations that sound natural, not robotic. Generative AI also uses context from previous interactions and retrieves relevant information from multiple internal systems.

This shift unlocks better digital banking user experience in four important ways.

1. Natural Conversations

Consider a corporate client asking, “Why did my bulk upload fail?”

A scripted bot replies: “Here is a guide on how to perform bulk uploads.” This provides no value. The client knows how to do it; they want to know why this specific attempt failed.

A Generative AI agent, using Retrieval-Augmented Generation (RAG) connected to the core banking logs, replies: “I see you attempted a bulk upload of 500 records at 9:00 AM. It failed because row 42 contains an invalid IBAN. Would you like me to correct the format or skip that row?”

This level of support solves the problem immediately. It reduces the load on the human support team and increases trust in the digital platform. It turns a moment of frustration into a demonstration of competence.

Generative AI can also:

- Interpret voice queries

- Understand ambiguous phrasing

- Handle multilingual or mixed-language input

- Maintain context across multiple questions

This is critical in African markets where customers often communicate in hybrid languages or blend English with indigenous languages.

In diverse markets like Nigeria, digital banking user experience depends on accessibility. Scripted bots struggle with local dialects, Pidgin, Hausa, or Yoruba. They fail to parse code-switching (mixing languages within a sentence).

Generative AI models trained on local datasets handle these linguistic nuances fluently. A customer can type, “I wan check my balance, abeg,” and the system understands the request, authenticates the user, and provides the information in the same dialect. This inclusivity opens digital banking to millions of previously underserved customers who may not be comfortable with formal English banking terminology.

2. Contextual Financial Advice

Instead of answering a question literally, generative models infer the reason behind the question. If a customer asks about a low balance, the model can check recurring deductions or highlight upcoming bills.

3. End-to-End Task Completion

Generative AI can trigger workflows such as:

- Requesting statements

- Blocking cards

- Setting savings goals

- Starting a loan application

This removes the need for customers to navigate long menus or fill out multiple forms.

4. Staff Augmentation

Internal teams gain value from generative AI as well. It summarises cases, drafts responses, and surfaces relevant policies. Teams resolve issues faster and reduce repetitive work.

This is the core of generative AI in finance. It does not replace teams. It improves their ability to deliver precise and consistent support across all channels.

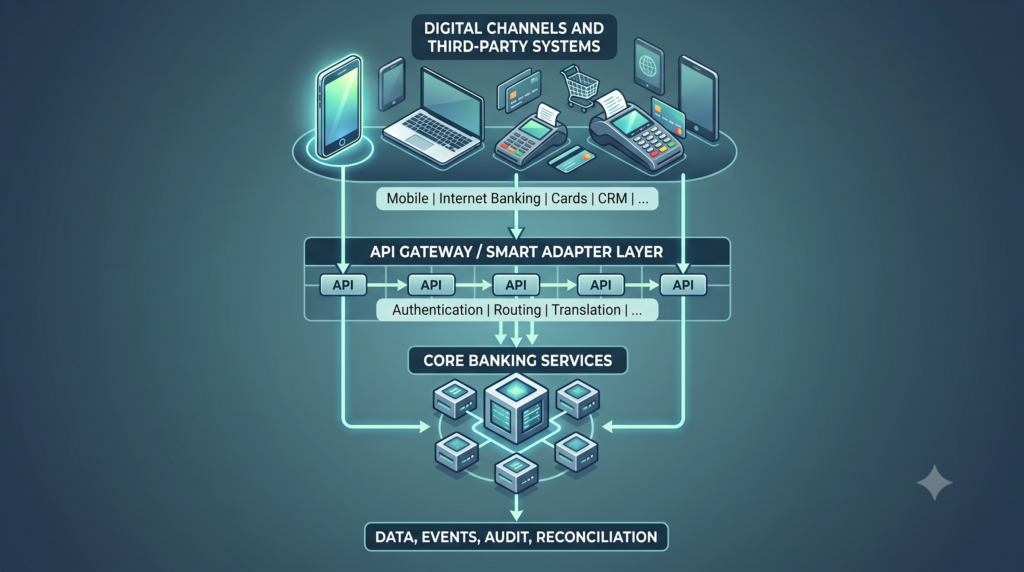

The Data Foundation: Infrastructure Before Intelligence

AI is only as good as the data it consumes. Many banks in emerging markets aspire to deploy AI but remain shackled by legacy infrastructure. Their data lives in silos. The card management system does not speak to the loan origination system. The mobile app data is separate from the branch data.

You cannot build true intelligence on fragmented data. Implementing AI in banking requires a modern data architecture. This involves three key steps:

- Data Unification: All transaction, interaction, and operational data must flow into a central data lake or warehouse. This provides the “single source of truth” required for training accurate models. Without this, your AI models will be biased or incomplete.

- Real-Time Processing: AI needs live data. Batch processing that updates once a day is insufficient for fraud detection or personalized offers. The core banking architecture must support event-driven streams. When a customer swipes a card, the AI must see that event in milliseconds, not tomorrow.

- API-First Design: AI agents need to take action. An insight is useless if the system cannot execute a task. Modern core banking software, like SeaBaas, exposes every function via API. This allows AI agents to initiate transfers, block cards, or adjust limits autonomously based on their analysis.

Case Studies: Personalized Banking in Emerging Markets

Artificial intelligence is already reshaping how banks across Africa operate. Below are three real patterns observed across the region.

Case Study 1: Intelligent Credit Expansion in East Africa

A mid-sized East African bank introduced behavioural scoring models to support MSME lending. Instead of relying solely on historical financial statements, the system analysed transaction patterns, business seasonality, and customer cash flow. Approval time fell significantly, and the bank reached new customer segments without raising risk.

Case Study 2: Proactive Fraud Alerts in Nigeria

A Nigerian digital bank integrated predictive fraud models linked to device telemetry. The system detected anomalous login attempts and intervened automatically before fraudulent transfers were initiated. Fraud losses decreased, and customers reported stronger trust in digital channels.

Case Study 3: Conversational Banking in North Africa

A North African institution deployed a generative AI assistant across its mobile channels. Customers used natural language to request statements, manage savings, and troubleshoot issues. Support tickets reduced, and digital adoption increased among older customers who previously preferred branches.

These examples illustrate a consistent theme. Institutions that invest in intelligence create stronger customer loyalty and more effective internal teams.

The Implementation Roadmap for CTOs

Transitioning from legacy systems to AI-driven banking is a significant undertaking. It requires a strategic roadmap.

Phase 1: Clean the Core Before deploying models, ensure your core banking system enables data access. If your core is a “black box” that only exports end-of-day reports, AI adoption will fail. You need a core like SeaBaas that supports open APIs and real-time data streams.

Phase 2: Identify High-Value, Low-Risk Use Cases Start with internal efficiency. Automating reconciliation or IT operations (AIOps) delivers immediate ROI with low regulatory risk. Once the organization trusts the AI, move to customer-facing applications like credit scoring.

Phase 3: Human-in-the-Loop Deploy AI as a “Copilot” first. Let the AI suggest a loan decision, but keep a human credit officer for the final approval. This allows the model to learn and allows the bank to verify accuracy before granting full autonomy.

Phase 4: Full Autonomy Once models prove stable and accurate, enable full agentic workflows for standard processes. Allow the AI to approve small loans, block fraudulent cards, and answer routine queries without human intervention.

The Economic Imperative

Adopting true AI is not merely a technical upgrade; it is an economic imperative. Banks with high operational costs and low customer satisfaction will lose market share to agile fintechs and digital-first challengers.

Banking process automation driven by AI reduces the cost-to-serve by 30% to 50%. It allows banks to scale their customer base without a linear increase in headcount. For institutions with Pan-African ambitions, this scalability is the key to profitable expansion.

Furthermore, the regulatory landscape is tightening. Central banks in Nigeria and the UAE are enforcing stricter compliance regarding AML (Anti-Money Laundering) and consumer protection. AI compliance tools are the only way to monitor millions of daily transactions effectively. Manual compliance teams cannot keep up with the volume or the sophistication of modern financial crime.

Stop Building Scripts. Start Building Intelligence.

The era of the “dumb chatbot” is ending. Customers demand intelligent, proactive, and context-aware banking experiences. They expect their bank to protect them from fraud, predict their financial needs, and speak their language.

For decision-makers, the path forward involves looking beyond the surface-level appeal of generative text. It requires investing in the deep infrastructure that makes intelligence possible. It means choosing core banking partners that prioritize data accessibility and real-time processing.

Peerless builds this intelligence into the foundation of our software. SeaBaas is not just a ledger; it is an AI-ready core banking system designed for the data intensity of the future. Kusala automates complex workflows, allowing your team to focus on strategy.

The future of banking belongs to institutions that can think, not just compute.

Discover SeaBaas’s AI-ready core architecture.

Image source: credgenics.com