The banking landscape in emerging markets is undergoing a critical shift. Driven by rapid technological advancements and a unique set of economic opportunities, financial institutions in Nigeria, Kenya, Egypt, and the UAE are leapfrogging traditional developmental stages. As we look toward 2026, the focus is no longer just on access to banking, but on the intelligence, speed, and autonomy of financial services. For banks and fintechs operating in these dynamic environments, understanding these shifts is survival. Here are the 10 trends that will define the next era of banking.

1. The Rise of “Agentic AI” in Operations

We are rapidly moving past the era of simple chatbots that can only answer frequently asked questions. By 2026, the industry standard will be “Agentic AI”—autonomous intelligent agents capable of executing complex workflows with minimal human intervention. In the back office, these agents will handle end-to-end tasks such as reconciling failed transactions, processing loan exceptions. They will also be negotiating payment plans with delinquent borrowers. In markets where skilled talent is often scarce and operational costs are high, these agents act as a scalable, 24/7 workforce that allows banks to grow without exponentially increasing their overhead.

2. Hyper-Personalization at Scale

Generic, “one-size-fits-all” banking is becoming obsolete. Financial institutions are leveraging generative AI to create a “segment of one,” where every customer interaction is unique. By 2026, a banking app will do far more than display a balance. It will predict financial shortfalls based on spending habits and proactively offer solutions, such as a micro-loan, before the user even realizes the need. This shift moves banking from a reactive utility to a proactive financial partner. This makes personalization the primary driver of customer retention.

3. Next-Gen Fraud Detection (AI vs. AI)

As digital transaction volumes explode, so do the sophistication and frequency of cyber threats. Hackers are already using AI to clone voices and bypass standard biometric checks. In response, banks are deploying AI-driven defense systems that go beyond static passwords. These systems analyze behavioral biometrics—such as typing speed, swipe patterns, and device handling—in real-time to detect anomalies. It is an arms race of AI versus AI, where security depends on the ability to identify subtle behavioral deviations that traditional rule-based systems would miss.

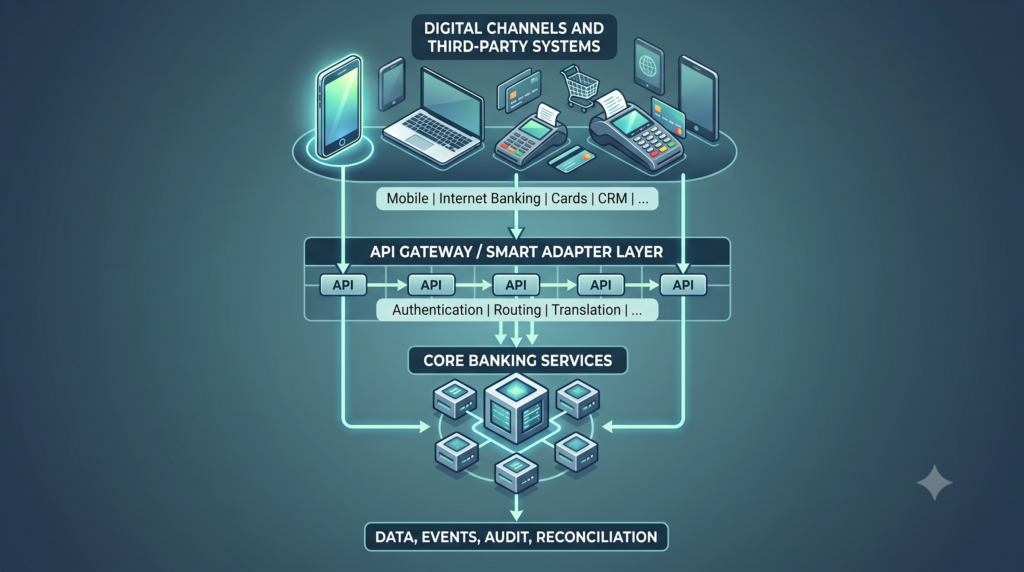

4. Cloud-Native Becomes the Default

The migration to the cloud is accelerating to the point of inevitability. By 2026, running an on-premise core banking server will be viewed as a significant liability rather than a security asset. Cloud-native platforms offer the elasticity needed to handle massive transaction spikes during peak periods and the agility to launch new products in days rather than months. For banks in emerging markets, this shift is critical for competing with agile fintechs that were born in the cloud and carry none of the legacy infrastructure baggage.

5. Embedded Finance 2.0 (The B2B Shift)

Embedded finance is evolving beyond consumer-focused “Buy Now, Pay Later” options at checkout. The new wave is distinctly B2B-focused. Logistics platforms will increasingly embed working capital loans for drivers, while agricultural marketplaces will integrate insurance directly for farmers. Banking is becoming invisible, integrated seamlessly into the platforms where business actually happens. This allows financial institutions to reach SMEs at the point of need, lowering acquisition costs and accessing rich data for underwriting.

6. Data Modernization as a Strategic Imperative

To fuel AI and personalization initiatives, banks require clean, accessible data. The era of siloed information—where card data sits separately from loan data—is ending. Banks are aggressively adopting “Data Fabrics” that provide a unified, real-time view of the customer across the entire organization. This modernization ensures that when an AI agent interacts with a customer, it has the full context of their financial life, leading to better decisions and smoother experiences.

7. Stablecoins for Cross-Border Trade

In markets often plagued by currency volatility and foreign exchange scarcity, stablecoins are becoming essential rails for B2B trade. By 2026, regulated stablecoins will likely be widely used for cross-border settlement by SMEs, allowing them to bypass slow and expensive correspondent banking networks. This shift reduces the friction of international trade, enabling local businesses to pay suppliers in China or Europe instantly and with lower fees.

8. Financial Inclusion 2.0: From Access to Empowerment

Having largely solved the challenge of “access” through the proliferation of accounts and wallets, the focus is shifting to “empowerment.” The next generation of tools will help the underbanked build wealth through automated micro-savings, fractional investing, and credit-building tools. These platforms will use alternative data, such as mobile usage patterns, to score the “invisible” customers who lack formal credit histories, bringing them fully into the economic fold.

9. The “Phygital” Branch Evolution

Despite the digital surge, the physical branch is not dying; it is evolving. Branches in emerging markets are transforming into advisory hubs dedicated to high-value interactions, such as mortgage consultations and SME business planning. Meanwhile, 99% of routine cash and service transactions are moving to digital channels or agent networks. This “phygital” model combines the trust and relationship-building of physical presence with the efficiency of digital operations.

10. ESG Integrated into Credit Scoring

Environmental, Social, and Governance (ESG) scores are moving from corporate reports to credit decisions. Banks are starting to offer lower interest rates to SMEs that adopt green practices, such as solar power installation or waste reduction. This effectively uses credit as a lever to drive sustainable development, aligning financial incentives with broader environmental goals and meeting the demands of socially conscious investors.

Building the Bank of 2026

The winners of 2026 will not necessarily be the biggest banks, but the most agile. They will be the institutions that embrace composable banking; using API-first platforms to snap together the best lending, payments, and compliance modules. Whether you are a microfinance bank looking to scale or a fintech building the next unicorn, the technology choices you make today will define your place in this future.

To navigate this transition, you need infrastructure that is built for speed and intelligence. SeaBaas provides the cloud-native core necessary to innovate without limits. Kusala offers the intelligent workflow automation to deploy agentic capabilities across your operations.

As your institution navigates 2026, our in-house experts can help map these trends to your current systems and identify practical next steps.

Book a clarity session with us to assess readiness, surface constraints, and explore how SeaBaas and Kusala can support your roadmap.