Introduction: Regulation Is No Longer a Periodic Event

In the Nigerian financial sector, the only constant is the next circular. For bank executives in Lagos, regulatory change is no longer a quarterly event; it is a continuous, high-velocity stream. From revised capital requirements to updated Know Your Customer (KYC) tiers and new open banking directives, the Central Bank of Nigeria (CBN) moves fast to stabilize and modernize the economy. However, the operational reality for many banks is a struggle to keep pace.

The bottleneck is rarely the compliance team; it is the infrastructure. Most institutions still run on rigid, foreign legacy cores designed for stable, slow-moving markets. For these systems, a new policy is not a simple update—it is a major change request. It involves logging a ticket with a vendor in Europe or Asia, waiting for a quote in foreign currency, and enduring a development cycle that can take months. By the time the update is deployed, the deadline has often passed.

This creates a dangerous operational gap. Sustainable CBN regulatory compliance for Nigerian banks cannot be achieved simply by hiring more staff to perform manual workarounds. To manage core banking compliance in Nigeria effectively, institutions need a fundamental shift in technology. It requires deploying an agile core banking platform that treats regulation as a simple configuration setting, not a complex code rewrite. This article explores how regulation is reshaping banking operations, why legacy cores continue to fail under regulatory pressure, and how modern, Nigerian-built platforms are changing the compliance equation.

Understanding the Nature of CBN Regulations Today

To navigate the current regulatory landscape, bank executives must first accept a fundamental shift: the CBN has moved beyond setting broad policy frameworks to policing the minute operational details of banking. The days of ambiguous guidelines are over. Today’s regulations are data-driven, technology-specific, and enforce immediate operational consequences.

Why CBN Regulatory Expectations Keep Expanding

The expansion of CBN supervision is driven by three core mandates that have evolved significantly between 2024 and 2026:

- Aggressive Consumer Protection: The CBN’s recent draft guidelines requiring mandatory 48-hour refunds for failed electronic transactions (October 2025) signal a zero-tolerance approach to operational inefficiency. It is no longer enough to have a dispute resolution team; banks must now have automated reconciliation systems that can beat the 48-hour clock or face automatic sanctions.

- Systemic Risk Management via Tech: With the introduction of the Baseline Standards for Automated AML Solutions (May 2025), the regulator now dictates how you manage risk. The requirement for AI-driven anomaly detection and real-time sanctions screening means that risk management is now a software engineering challenge, not just a policy document.

- Financial Stability & Surveillance: Through initiatives like the Electronic Foreign Exchange Matching System (EFEMS) and the Payments System Vision 2025, the CBN is demanding granular visibility into the financial system. They don’t just want to know that a transaction happened; they want the geo-location of the POS terminal and the ISO 20022 messaging standard attached to it.

Compliance Is Now Operational, Not Just Legal

For decades, compliance was a legal function—a team of lawyers reviewing circulars. Today, compliance is an operational and technical function. A legal opinion cannot code a new GSI trigger or re-configure a transaction limit.

- Product Design: When the CBN updates Tiered KYC limits (as seen in recent circulars), your core banking system must instantly enforce these new caps across all channels. If your system requires hard-code changes to update a Tier 1 savings limit, you are operationally non-compliant the moment the circular goes live.

- Transaction Processing: The mandate for mandatory geo-tagging of POS terminals (September 2025) fundamentally changes how transactions are processed. Your switch and core must now be able to validate latitude/longitude data fields in real-time, rejecting transactions that fall outside the approved geofence. This is a technical hurdle that legacy cores struggle to clear without expensive customization.

- Reporting Frequency: Daily reporting for Fintechs and PSPs makes manual Excel aggregation impossible—compliance now requires automated data flows. Compliance now requires an API-first core that automatically pushes data to regulators, not manual pulls and formatting.

- Audit Readiness: GSI audit trails must prove what was recovered, when triggers fired, and how the system identified qualifying accounts. This requires a system that logs every decision logic, making audit readiness a default state rather than a frantic preparation.

The High Cost of Regulatory Lag

In the current Nigerian banking environment, speed is a compliance metric. The cost of failing to adapt to a new CBN directive immediately is no longer just a slap on the wrist; it is an existential threat.

The financial penalties have escalated significantly, but the reputational and strategic costs are often far higher. Beyond monetary fines, the CBN has shown a willingness to deploy severe sanctions for non-compliance, including the suspension of specific banking licenses, restrictions on access to the foreign exchange window, or even the removal of key board members. For a bank, being locked out of the FX market or having a product line suspended due to a compliance lag is a revenue disaster that far outweighs the cost of any software upgrade.

Furthermore, the operational drag of regulatory lag is a silent killer of efficiency. Consider the implementation of the Global Standing Instruction (GSI). When this policy was introduced, banks running on rigid legacy cores could not automate the recovery trigger immediately. Instead, they were forced into “manual compliance”—deploying teams of staff to manually track, calculate, and debit accounts across other institutions. This manual workaround is not only expensive and slow; it introduces a high margin for human error, increases staff fatigue, and ultimately leaves the bank vulnerable to further audit queries.

The Real Compliance Burden Nigerian Banks Face

The shift in supervisory style has exposed the deep structural weaknesses of legacy banking infrastructure. For compliance officers and CTOs, the daily reality involves fighting fires on two fronts: the complexity of reporting and the crushing cost of maintaining rigid systems.

Reporting Complexity and Frequency

The era of submitting a static monthly Excel file for eFASS (Electronic Financial Analysis and Surveillance System) is ending. The CBN now demands high-velocity, granular data—often in real-time. Whether it is daily AML transaction monitoring or the geo-location tagging of POS terminals, the regulator wants raw data, not summaries.

For banks running on legacy cores, this is a nightmare. Data is often trapped in fragmented silos—loans in one database, deposits in another, and trade finance in a third. Compliance teams are forced to manually export, clean, and aggregate this data to meet submission deadlines. This manual “Excel gymnastics” introduces data inconsistencies, leading to regulatory queries and fines for misreporting, simply because the core system cannot provide a “single source of truth.”

Cost of Compliance on Legacy Systems

The financial cost is equally punishing. On a foreign legacy core, Nigerian regulations are treated as “customizations.” Every time the CBN issues a circular changing a policy limit (e.g., a new FX bidding cap), the bank must pay its foreign vendor in USD to modify the hard-coded logic.

This creates a “Vendor Trap.” Banks are forced to wait months for simple configuration changes, surviving on risky manual workarounds in the interim. The result is a bloated IT budget where up to 40% of spend goes towards keeping the lights on and retrofitting the system for compliance, rather than innovating for the customer.

Why Legacy Core Banking Systems Struggle with CBN Compliance

The biggest obstacle to CBN regulatory compliance for Nigerian banks is not the regulation itself, but the software running the bank. A core banking system originally built for the stable markets of Europe or North America often views Nigerian regulatory dynamism as a deviation and treats mandatory local rules as expensive customizations.

This creates a broken workflow known as the “Vendor Bottleneck.” When the CBN issues a new directive with an immediate deadline, the bank must contact its foreign vendor, wait for a change request quote in USD, and then wait further for the vendor to slot the update into a global product roadmap. This timeline, often stretching weeks or months, is fundamentally incompatible with the CBN’s demand for immediate compliance. Consequently, banks are forced to burn scarce FX on constant software maintenance while risking penalties for non-compliance.

Rigid Architecture That Slows Regulatory Response

Legacy cores were built for stability, not adaptability. In these systems, regulatory logic is often hard-coded deep within the application. Changing a transaction limit or a KYC tier requires actual code rewriting, long release cycles, and scheduled downtime windows. Modern compliance requires agility—the ability to change rules via configuration without rebooting the bank.

Fragmented Data and Poor Audit Trails

The CBN increasingly demands full traceability and “single source of truth” reporting. Legacy systems, however, often store data in fragmented silos (e.g., trade finance separate from core deposits). This lack of a unified data fabric makes automated reporting impossible and leaves audit trails incomplete, forcing compliance teams to manually gather evidence during examinations.

Dependence on Foreign Vendors for Local Rules

Most foreign platforms do not natively support Nigerian regulatory logic. Banks remain dependent on vendors who may lag behind local regulatory changes, weakening core banking compliance in Nigeria and driving up long-term costs.

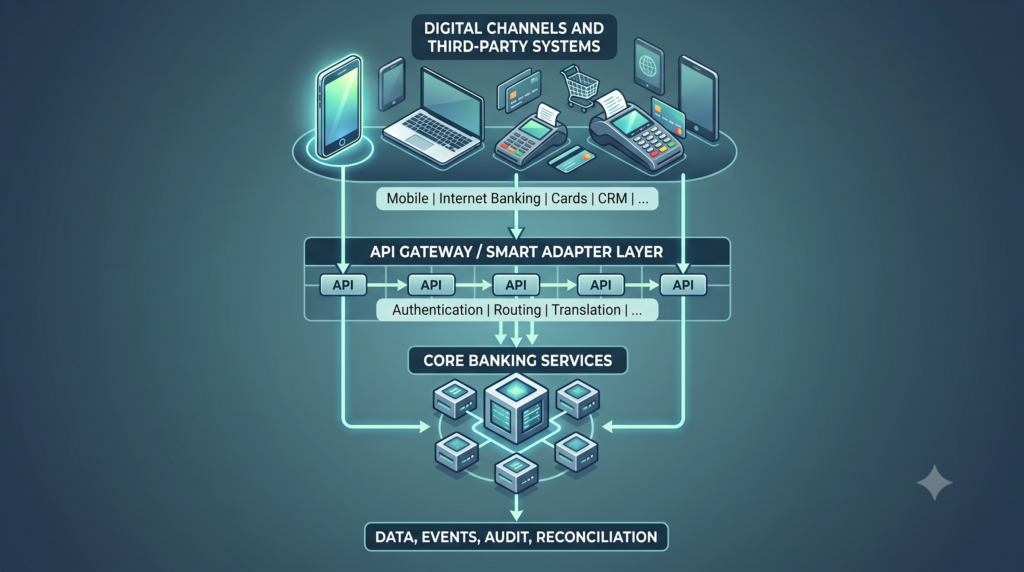

What Makes an Agile Core Banking Platform Compliance-Ready

To survive the current regulatory velocity, Nigerian banks must pivot from rigid legacy structures to agile architectures. An agile banking platform is not just faster; it is fundamentally designed to treat compliance as a variable, not a constant.

Configurability Over Custom Code

The defining characteristic of a modern core banking system in Nigeria is the separation of business logic from the core code. In a legacy system, a new CBN directive—such as changing the maximum withdrawal limit for a Tier 1 account—often requires a developer to rewrite code and redeploy the application.

In an agile system, this is a configuration setting. Compliance officers or authorized administrators can adjust transaction limits, fee structures, and KYC parameters via a dashboard in minutes. This capability eliminates the need for expensive vendor change requests and allows the bank to achieve regulatory compliance immediately upon the release of a circular.

Real-Time Data and Automated Reporting

Speed is the new standard. The CBN’s move towards near real-time supervision requires a system that captures data instantly. Unlike legacy systems that rely on end-of-day batch processing, agile platforms are event-driven. Every transaction updates the General Ledger in real-time.

This “single source of truth” enables automated regulatory reporting. Banks can generate complex reports like eFASS returns with a single click, confident that the data is accurate and up-to-the-second. This drastically reduces the operational risk associated with manual reconciliation and ensures that the bank is always audit-ready without the need for frantic end-of-month data cleaning.

The Advantage of a Localised Core Banking Platform in Nigeria

Running a core banking system built specifically for this market gives you a distinct “Home-Court Advantage,” rather than adapting a generic global platform to fit local realities.

Built with Nigerian Regulations in Mind

A localized core banking platform is proactive, not reactive. While foreign providers view Nigerian mandates as edge cases, a local platform treats them as foundational requirements. Critical compliance features such as direct NIBSS integration, GSI triggers, and Credit Bureau reporting modules are native to the system. They are built-in, not expensive “bolt-ons.” This means the system logic naturally aligns with CBN reporting structures and nuances from Day One.

Lower Cost of Compliance Over Time

The economic argument is undeniable. Relying on foreign vendors exposes banks to volatile FX rates and unpredictable “professional services” fees in USD. Every regulatory update becomes a negotiation. In contrast, a localized platform drastically reduces the Total Cost of Ownership (TCO). Pricing is predictable and in Naira, eliminating FX exposure. Furthermore, because compliance updates are part of the standard roadmap, banks avoid the endless cycle of paying customization fees just to remain legal.

Faster Regulatory Alignment

Agility is a function of proximity. Local technology partners operate in the same time zone and read the same CBN circulars as their clients. The feedback loop between a regulatory announcement and a software update is immediate. While a foreign vendor might deprioritize a Nigerian policy change, a local partner aligns their development sprints directly with CBN regulations for banks, ensuring that your platform adapts as fast as the regulator does.

How a Modern Core Turns Compliance into a Competitive Advantage

In an environment defined by volatility, the ability to adapt instantly is not just a defense mechanism; it is a competitive edge. While competitors scramble to patch legacy systems, banks running on an agile banking platform can pivot immediately, turning regulatory adherence into a marker of operational excellence.

Consider the monthly ritual of submitting returns. For many, this is a week-long struggle of manual Excel aggregation. With a modern core, the system automatically generates CBN monthly returns (eFASS). The system pulls data directly from a unified general ledger, eliminating the risk of manual errors and freeing up staff for strategic tasks.

Similarly, agility transforms how banks handle policy shifts. If the CBN issues a directive changing the maximum withdrawal limit for Tier 1 accounts, an agile bank does not wait for a vendor patch. Administrators simply update the parameter via a dashboard in minutes. This specific flexibility is the defining feature of effective compliance software—it ensures that your operations reflect the law in real-time.

Faster Product Approvals

Compliance readiness directly impacts speed-to-market. Banks with agile cores can launch new products faster because they bake compliance controls into the design phase. When you can demonstrate to the regulator that a new savings product has automated KYC triggers and built-in transaction limits, regulatory approval becomes a smoother, faster process.

Stronger Trust with Regulators and Customers

Ultimately, consistency builds capital. A bank that consistently submits accurate, timely reports attracts fewer audits and regulatory sanctions. Better reporting and perpetual audit readiness lead to fewer findings during examinations, enhancing institutional credibility with both the Central Bank and the investing public.

SeaBaas and Regulatory Readiness in Nigeria

When analyzing the technology landscape, the distinction between a “globally adapted” system and a “locally engineered” one becomes critical. SeaBaas stands out as a cloud-native, agile banking platform designed with Nigerian regulations at its foundation.. It functions less like a vendor product and more like a compliance partner, transforming the relationship between the bank and the regulator from adversarial to collaborative.

Designed for Nigerian Banking Operations

We built SeaBaas with the fundamental understanding that in Nigeria, flexibility is survival. It replaces the rigidity of legacy code with configurable workflows. Whether a bank needs to adjust daily transaction limits to align with a new CBN directive or re-configure KYC requirements for a specific product tier, operations teams can execute these changes instantly via a user-friendly interface. This modularity drastically reduces compliance friction, allowing banks to focus on serving customers rather than fighting their own infrastructure.

Compliance-Friendly Architecture

True compliance requires absolute visibility. SeaBaas features a compliance-friendly architecture built on real-time reporting capabilities and granular role-based access controls. Every transaction and administrative action within the system generates a built-in, immutable audit trail. This ensures that when examiners arrive, the bank can produce accurate, comprehensive evidence of compliance immediately, without the need for frantic manual data gathering.

Cost-Effective Alternative to Foreign Cores

Finally, the economics of compliance must change. SeaBaas offers a sustainable, cost-effective alternative to foreign legacy cores. By eliminating the need for expensive, dollar-denominated customization fees for standard regulatory updates, it drastically lowers the cost of staying compliant. With a local support team that monitors CBN circulars alongside you, the platform evolves with the market, ensuring better long-term compliance economics.

How Nigerian Banks Can Prepare for the Next Wave of CBN Regulations

As the regulatory environment in Nigeria continues to accelerate, bank executives must move beyond reacting to yesterday’s circulars and start preparing for tomorrow’s mandates. Future-proofing your institution requires a proactive assessment of your technology stack’s agility.

Assess Core Banking Flexibility

The first step is a rigorous internal audit of your current capabilities. Bank leaders should ask two critical diagnostic questions:

- “What is our Time-to-Compliance?” When the CBN issues a new directive (e.g., a change in Maximum Cumulative Balance for a Tier 3 wallet), how many days or weeks does it take to reflect this change in the core system? If the answer is measured in months, your license is at risk.

- “How manual is our reporting today?” If your compliance team spends the first five days of every month aggregating Excel spreadsheets from disparate departments to meet eFASS deadlines, your operational risk is dangerously high. A modern core should automate this process entirely.

Prioritise Systems That Adapt, Not Just Comply

Strategic preparation means prioritizing systems that offer adaptability as a native feature, not a paid add-on. Investing in a core banking platform that requires a change request for every minor regulatory adjustment is a short-term fix with long-term consequences. Instead, banks must prioritize agile banking platforms that allow internal teams to configure rules instantly. By choosing technology that adapts at the speed of the market, you transform regulation from a disruption into a routine operational variable.

Conclusion: Compliance Is a System Decision

In the final analysis, regulatory volatility is a constant in Nigeria. The Central Bank of Nigeria (CBN) will continue to evolve its mandates to ensure stability and consumer protection. For bank executives, the choice is clear: you can either fight this reality with rigid legacy systems that increase cost and operational risk, or you can embrace it with agile, localised platforms that reduce friction.

Your core banking system should be a shield that protects you, not a burden that slows you down. Achieving sustainable core banking compliance in Nigeria is ultimately an infrastructure decision. Moving to a localized, agile platform like SeaBaas is the most effective strategy for long-term compliance and cost management.

CBN compliance does not have to slow your bank down.

Future-proof your compliance strategy today. Stop paying dollar rates for slow regulatory updates and manual workarounds. Switch to a core that moves as fast as the market.

Book a Clarity Session with Peerless to assess how agile your current core banking system is and explore how platforms like SeaBaas support faster, lower-cost regulatory compliance in Nigeria.