The velocity of the Nigerian financial services sector is nothing short of breathtaking. If you look at the NIBSS transaction data from the last 24 months, the trajectory is vertical. We are seeing an explosion in transaction volumes, a surge in digital-first customer acquisition, and an aggressive entry of neobanks that play by entirely different rules.

For Chief Technology Officers (CTOs) and bank executives in Lagos, this growth is a double-edged sword. On one side, the market opportunity is immense. On the other, the operational reality is terrifying.

Many established financial institutions are attempting to win this race while driving a 1990s sedan. They are shackled by monolithic, on-premise legacy systems that were designed for a different era of banking—an era where “end-of-day processing” was acceptable and mobile apps were an afterthought.

Today, the “Legacy Anchor” is real. It manifests as downtime during salary weeks, the struggle to integrate with new fintech partners, and the agonizingly slow rollout of new products.

The shift from Legacy to Modernisation

Nigerian banks are being judged by speed and reliability. Customers expect instant transfers, always-on channels, transparent fees, and service that does not depend on branch visits. Regulators expect stronger controls, better reporting, and operational resilience that protects the financial system. Partners expect clean APIs that make integration predictable.

In this environment, cloud-native core banking in Nigeria is becoming the foundation for banks that want to launch products faster, reduce downtime, and compete more effectively with agile fintechs. Many institutions already host parts of their stack on the cloud, but hosting is not the same as cloud-native. A cloud-native core is designed to scale cleanly, change safely, and integrate quickly.

This guide breaks down what “cloud-native” should mean in practice for Nigerian banks, what outcomes to expect, and how to evaluate platforms. It also shows why SeaBaas is positioned as a modern core for institutions across tiers and categories, from microfinance banks to larger players building next-generation financial services.

Cloud-native core banking in Nigeria is no longer optional for growth

Banks in Nigeria are not only competing with other banks. They are competing with product experiences across fintech apps, super apps, and digital-first consumer services. The market’s tolerance for friction keeps shrinking. When onboarding takes too long, when transfers fail intermittently, or when support cannot resolve issues quickly, customers switch.

At the same time, costs are rising. FX pressure impacts technology procurement. Infrastructure investment must be justified. Teams are leaner, yet service expectations keep expanding. A modern core becomes a business requirement because it directly shapes revenue velocity, customer retention, and operational cost.

Customer expectations now reward speed and reliability

Digital banking user experience now depends on consistency. Customers do not separate “core banking” from “mobile app.” They experience the bank as one system. If your core processes batch updates overnight, customers experience delays in balances, limits, loan status, and dispute outcomes. If your system struggles during peak periods, customers experience it as unreliability.

Cloud-native cores are built to deliver real-time processing, elastic scalability, and cleaner integration with channels. This is how modern institutions reduce friction and retain customers in competitive corridors such as retail, SME, and agent banking.

Regulation and reporting needs are increasing operational load

Compliance and reporting are not side tasks. They shape how banks operate daily. When data is fragmented, reporting becomes manual. Manual processes create errors. Errors create risk. A cloud-native core with strong audit trails, consistent data models, and clear permissioning reduces the operational drag of compliance and supports better governance.

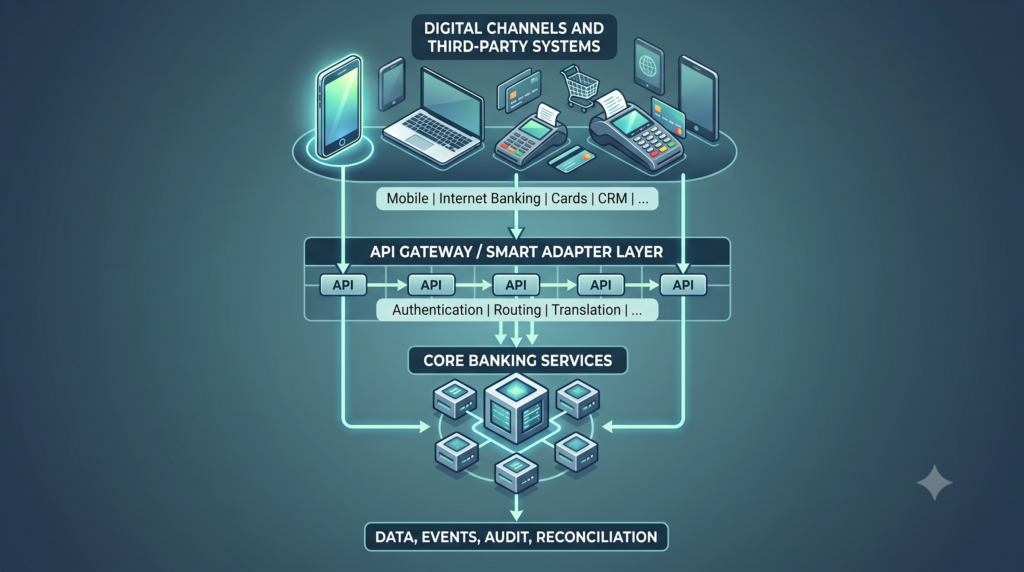

What “cloud-native” should mean for a Nigerian bank

Many platforms market themselves as “cloud” because they can be hosted on cloud infrastructure. That is not enough. For banks evaluating cloud-native core banking in Nigeria, the more useful question is this: does the system change and scale like a modern platform, or does it behave like legacy software running in a new location?

A practical cloud-native definition for banking should include microservices, elastic scaling, API-first integration, and real-time data visibility.

Microservices architecture that supports change without disruption

A cloud-native core should be modular, with services that can be updated without destabilising the entire platform. This reduces the risk and disruption that typically comes with upgrades and change cycles. It also allows banks to improve specific capabilities without waiting for monolithic release windows.

For product teams, this translates to faster iterations. For technology leaders, it translates to safer releases. And for operations, it translates to fewer periods of instability during change.

Elastic scalability for peak demand without performance drop

Nigeria experiences transaction peaks that can stress systems, especially during salary periods, festive seasons, and promotional campaigns. A cloud-native system should scale based on demand, not based on pre-purchased capacity that sits idle most of the year.

Elastic scalability keeps performance consistent during peaks and supports growth without repeated infrastructure rebuilds. It also helps banks manage costs because capacity can be planned more intelligently.

API-first integration with Nigeria’s rails and partner ecosystems

Banks in Nigeria are not operating alone. They integrate with payment rails, switches, regulators, fintech partners, aggregators, and internal enterprise systems. An API-first core shortens integration timelines and reduces the hidden cost of bespoke middleware.

API-first also makes partnerships easier. It supports faster launches of digital products that depend on external services, including risk scoring, payments, identity verification, and customer engagement platforms.

Real-time core-to-channel data and cleaner reconciliation

Modern banking depends on real-time visibility. A cloud-native core should support event-driven data flows that reduce the need for manual reconciliation and constant exception handling. When balances, limits, and transaction status update instantly across systems, customer support improves, dispute resolution gets faster, and finance teams spend less time chasing data.

The business outcomes banks expect from a cloud-native core

Cloud-native technology is not an end goal. It is a means to business outcomes. Institutions modernise because they need to ship products faster, improve uptime, lower operational costs, and build a platform that supports continuous change.

1. Faster product launches without multi-year projects

A cloud-native core makes it easier to configure products and iterate without repeated heavy builds. This matters in Nigeria where banks need to respond quickly to new customer needs, evolving competition, and regulatory changes.

A modern core supports faster launches of savings products, SME lending, microcredit, agency banking features, and segmented offerings designed for specific customer groups. The goal is not simply “more products.” The goal is shipping products that match customer behaviour and business strategy without dragging the organisation into long, expensive projects.

2. Better uptime and reduced operational turbulence

Uptime is a brand promise. Downtime is not only a technology incident. It is a business interruption that affects trust, revenue, and reputation. Cloud-native systems are designed for high availability and resilient operations.

SeaBaas, in production usage, has demonstrated 99.95% availability. That level of reliability reduces the turbulence that drains operations teams and undermines customer confidence.

3. Lower total cost of ownership that shows up in cash flow

Banks in Nigeria live with cost constraints that are not theoretical. They are immediate. Legacy cores often carry high licensing costs, heavy infrastructure costs, and expensive change cycles.

A cloud-native core reduces infrastructure overhead, improves operational efficiency, and can lower the cost per transaction as volume scales. SeaBaas has contributed to $1m+ in operational savings for customers, reflecting the real financial impact of modernising the core foundation.

4. Performance that stands up to real transaction volume

Modern platforms are tested in production, not in presentations. SeaBaas processed over 2.5B+ transactions in 12 months, demonstrating reliability at high throughput. This matters for banks that need predictable performance under growth, peak periods, and expanding channel usage.

The real blockers to core banking modernisation in Nigeria

Many banks understand the need to modernise. The blockers are often practical, not philosophical. They include rigid legacy architectures, slow integrations, manual reporting workarounds, and change risk.

Rigid legacy architecture and long upgrade cycles

Legacy cores were designed for stability in a slower market. They often require long upgrade cycles, heavy vendor dependence, and high disruption risk. This slows product launches and limits continuous improvement. It also forces teams into workaround culture, where manual steps become normal.

Poor integration capability and slow partner launches

Fintech partnerships move fast. When core systems cannot expose reliable APIs, integrations become expensive and slow. Banks miss partnership windows, product ideas stall, and teams get trapped in custom builds that are difficult to maintain.

Reporting gaps and manual workarounds that increase risk

Manual reporting is a symptom of deeper issues. When the core cannot provide clean, consistent, real-time data, teams build spreadsheets. Spreadsheets create inconsistencies. Inconsistencies create risk. This cycle expands operational cost while increasing exposure.

SeaBaas in focus: cloud-native core banking built for Nigerian realities

SeaBaas was built to support banking operations in emerging markets like Nigeria with the reliability and configurability modern institutions require. It is cloud-native, API-first, modular, and designed to serve financial institutions across tiers and categories.

It fits banks that want to modernise without adopting a one-size-fits-all platform that ignores local realities.

Composable, configurable product engine

Product strategy should not be limited by the core. SeaBaas supports configuration-led setup so institutions can tailor products, fees, limits, and workflows to fit their operating model. This helps banks launch and refine offerings without repeated heavy builds.

For teams, this improves speed. For leaders, this improves strategic flexibility.

Core modules that cover the daily banking footprint

A modern core must cover the essentials without forcing banks into fragmented systems. SeaBaas supports key operational modules including customer management, credit management, ledger and accounting, reporting, user and role management, audit trail, and end-of-cycle processing. This provides the foundation banks need for daily operations and growth.

Built-in controls that support governance and auditability

Banks need systems that strengthen accountability. SeaBaas includes role-based access, permission-driven controls, and audit trails that support operational governance. This improves traceability for internal controls and reduces reliance on manual evidence gathering during reviews.

Designed to serve multiple institution types, not one category

SeaBaas is built to serve institutions irrespective of tier or category. Its modular design supports different banking models, from microfinance institutions running lean operations to larger banks managing multi-channel scale. The platform’s configurability allows each institution to align the system with its specific requirements rather than adapting the institution to the platform.

Proof of traction and resilience in production

SeaBaas is not positioned as a future promise. It is positioned as a system tested by real usage. 2B+ transactions processed in 12 months, 99.95% availability, and a 60% reduction in processing time show outcomes that matter to CTOs, operations leaders, and risk teams. These are the signals banks look for when evaluating core platforms in Nigeria.

Deployment options in Nigeria: SaaS, dedicated cloud, and on-prem

Banks in Nigeria do not all have the same constraints. Deployment flexibility matters because risk posture, data residency considerations, internal policies, and speed requirements vary by institution.

When SaaS makes sense for MFBs and digital challengers

For microfinance banks and digital challengers, SaaS can reduce time to value. It can shorten onboarding, reduce infrastructure overhead, and provide predictable operational costs. It also supports faster iteration because updates and improvements are managed centrally with clear governance.

This is where SeaBaas SaaS becomes a practical option for institutions that want a modern core without heavy infrastructure ownership.

When dedicated cloud or on-prem fits regulated constraints

Some institutions prefer dedicated deployments due to internal policies, risk posture, or regulatory considerations. SeaBaas supports flexible deployment approaches so banks can align technology choices with governance requirements while still adopting modern architecture and integration patterns.

How to choose a cloud-native core banking platform in Nigeria

Selecting a core banking platform is a strategic decision with long-term impact. A good evaluation framework helps banks avoid marketing claims and focus on what drives outcomes.

Architecture and scalability

Assess whether the system is truly modular, built for high availability, and designed for safe change cycles. Ask how scaling works in peak periods and how releases are managed. A cloud-native core should support growth without constant infrastructure redesign.

Integration readiness

Integration is where many projects slow down. Review API maturity, documentation quality, event support, and compatibility with banking standards. A modern core should reduce integration effort, not shift it elsewhere.

Product configuration speed

Ask how quickly teams can create and adjust products. Look for configuration-led design rather than hard-coded changes. Product agility is a competitive factor, especially against fintech competition in Nigeria.

Compliance posture and audit trails

A strong core supports compliance as a built-in capability, not an afterthought. Assess audit logs, permissioning, reporting readiness, and the ability to trace changes and transactions clearly.

Vendor model and delivery support

Modernisation success depends on delivery, not only software. Evaluate implementation support, governance, partner ecosystem, and how the vendor handles training and operational readiness. A modern core should come with a practical adoption model that fits your institution’s capacity.

Competitive landscape: what are the options?

Banks evaluating cloud-native core banking in Nigeria often compare global platforms and local alternatives. Global cores can be powerful but may come with cost structures and implementation complexity that do not always fit emerging-market realities. Local platforms may fit context better but vary in maturity and architectural strength.

The clearest way to navigate the landscape is to return to outcomes and fit. A modern core must deliver reliability, fast product configuration, integration readiness, and a deployment model aligned with your institution’s governance. SeaBaas is positioned for banks that want modern architecture with practical delivery in African markets.

FAQs

1. What qualifies as cloud-native core banking in Nigeria?

Cloud-native core banking in Nigeria should mean more than hosting software on a cloud server. It should include modular services, elastic scalability, strong APIs, event-driven data flow, and high availability that supports real-time banking. It should also support governance needs such as audit trails, permissioning, and reporting. If change cycles still require heavy disruption, the system is likely cloud-hosted rather than cloud-native.

2. What is the difference between cloud-hosted and cloud-native core banking?

Cloud-hosted systems are traditional applications running on cloud infrastructure. They may still behave like legacy systems, with rigid upgrades and limited scaling flexibility. Cloud-native cores are designed to scale dynamically, evolve through safer releases, and integrate easily through APIs and events. The difference shows up in product agility, uptime stability, and how quickly the bank can integrate new capabilities.

3. Can a cloud-native core meet CBN compliance expectations?

Yes, provided the system supports clear audit trails, strong controls, reliable reporting, and governance features that align with regulatory expectations. Compliance is often strengthened when institutions reduce manual processes and improve traceability. The key is selecting a platform with built-in governance capabilities and a deployment model that aligns with the institution’s data and security posture.

4. How long does core banking modernisation take with a modular platform?

Timelines vary based on scope, migration approach, and readiness. Modular platforms can reduce complexity through phased deployment, where banks modernise in stages rather than switching everything at once. A clarity-led approach helps define scope, prioritise high-impact areas, and reduce implementation risk.

5. What does SaaS core banking in Nigeria change for cost and rollout speed?

SaaS core banking can reduce infrastructure ownership and speed up time to deployment, especially for institutions that want predictable costs and faster onboarding. It can also simplify upgrades and support continuity when governed properly. For many MFBs and digital challengers, SaaS offers a faster path to modern core capabilities without heavy upfront infrastructure investment. Contact our experts to learn what SeaBaas Saas cost.

6. What integrations should a modern core support from day one?

At minimum, modern cores should integrate cleanly with digital channels, payment rails, identity and KYC tools, reporting systems, and partner ecosystems. API-first integration capability reduces friction and supports faster launches. Over time, the ability to integrate analytics, fraud detection, and workflow automation becomes equally important.

Book a clarity session

Modernising core banking in Nigeria becomes easier when the scope is clear. A clarity session maps your current constraints, target products, integration needs, compliance considerations, and the best deployment model. It ends with a practical path to move from legacy limits to cloud-native capability using SeaBaas. Whether you are looking to explore your options with SaaS and On-prem or you want a demo, you can book a clarity session with our experts here.

SeaBaas proof in production

SeaBaas has now processed 5B+ transactions, delivered 99.95% availability, reduced processing time by 60%, and contributed to $10m+ operational savings. If your institution wants a modern core built for scale in Nigeria, this is a practical starting point.