Traditional credit bureaus in Nigeria and Kenya capture less than 20% of economic activity. This creates a massive disconnect in the financial ecosystem. Lenders have capital to deploy, and Small and Medium Enterprises (SMEs) require working capital. Yet, lenders relying solely on bureau data reject creditworthy SMEs daily. This leaves significant revenue on the table.

The problem is not a lack of creditworthiness. It is a lack of visibility. The informal sector drives the African economy, but it generates data that traditional banking algorithms ignore. Credit scoring AI changes this dynamic. It analyzes transaction history, mobile data, and supply chain activity to assess risk accurately for businesses without formal credit history.

For Chief Risk Officers and Lending Product Managers, this shift represents the difference between stagnating portfolios and safe, profitable growth.

The Data Blind Spot in Traditional Lending

To understand the solution, we must first analyze the limitation of the current model. Traditional credit scoring relies on three pillars: historical repayment data, audited financial statements, and collateral.

In mature markets, this works. In emerging markets, it fails. Most SMEs operate in the informal or semi-formal economy. They transact in cash or via mobile money, and do not have audited financial statements from a major firm. They also rent their premises and lease their equipment, so they lack physical collateral.

When a loan officer applies traditional criteria to these businesses, the result is a rejection. The borrower is labeled “high risk” simply because they are “unknown.” This is a data blind spot. The borrower might have a thriving business with consistent cash flow, but that cash flow is invisible to the credit bureau. Consequently, it does not exist in the eyes of the bank.

This data blind spot creates the “SME Credit Gap,” estimated at over $330 billion across Africa. Closing this gap requires financial inclusion technology that sees beyond the blind spot.

Alternative Data: Scoring Credit Without a Credit Score

Artificial Intelligence succeeds where traditional models fail because it digests unstructured and alternative data. It constructs a risk profile from thousands of digital data points rather than a single credit report.

The Power of Mobile and Utility Data

In the absence of a formal banking history, mobile usage patterns serve as a strong proxy for creditworthiness. Alternative data credit scoring models analyze anonymized mobile data to determine stability and reliability.

Key indicators include:

- Airtime Top-up Patterns: A user who tops up airtime consistently every week demonstrates better cash flow stability than one who tops up sporadically.

- Data Usage: High data consumption often correlates with higher economic activity and digital literacy.

- Mobile Money Velocity: AI looks at the velocity of funds moving through a wallet. It analyzes how quickly money comes in and goes out, alongside the average balance over 30 days.

For an SME in Lagos, this means their business activity is finally recognized. The AI sees that they pay their suppliers via mobile transfer every Friday. It sees that they pay their electricity bill on the first of the month. It builds a “shadow credit score” that accurately reflects their financial discipline.

Supply Chain and Inventory Data

For larger SMEs, supply chain data provides an even richer source of truth. Many distributors use digital platforms to order inventory from manufacturers (FMCGs).

Credit scoring AI connects with these platforms. It analyzes order frequency to signal growth. It examines inventory turnover to measure operational efficiency. And it tracks return rates to identify operational instability.

Peerless understands that this data often sits in separate ERPs or spreadsheets. Our core systems ingest these disparate data streams. This allows lenders to underwrite loans based on verified trade activity rather than unverified financial statements.

Reducing Non-Performing Loans (NPLs) with Machine Learning

The primary concern for any Chief Risk Officer entering the SME market is a potential spike in Non-Performing Loans (NPLs). High interest rates in SME lending Nigeria act as a risk premium to cover high default rates.

AI helps originate more loans and helps reduce non-performing loans by monitoring risk in real-time.

From Static to Dynamic Risk Monitoring

Traditional loans are static. The bank assesses risk at origination, disburses the cash, and waits 30 days for the first repayment. If the borrower’s business collapses on day five, the bank does not know until day 30.

AI introduces dynamic monitoring. Once a loan is disbursed, the model continues to monitor the borrower’s transactional behavior.

Consider a merchant who typically processes N500,000 in daily sales through their Point of Sale (POS) terminal. If that volume drops to N50,000 for three consecutive days, the AI flags an anomaly. It alerts the risk team immediately.

This allows the bank to contact the customer to investigate potential terminal faults or supply issues. This proactive engagement often prevents a default before it happens. The bank might offer a temporary restructure or a payment holiday, protecting the principal.

Predicting “Can’t Pay” vs. “Won’t Pay”

Defaults happen for two reasons: ability (can’t pay) and willingness (won’t pay). Differentiating between the two is critical for collections strategy.

Machine learning models analyze behavior to predict which category a delinquent borrower falls into.

- The “Can’t Pay”: This borrower has stopped all transactions. Their business activity has ceased. Aggressive collections will yield nothing. The strategy here is restructuring or write-off.

- The “Won’t Pay”: This borrower is still transacting. They are paying suppliers and utility bills but ignoring the loan repayment. They have the funds but prioritize other expenses. The strategy here is immediate, firm enforcement.

By segmenting delinquent accounts automatically, AI ensures that collections teams focus their energy where it yields results. This significantly improves NPL recovery ratios.

The Economic Impact of Inclusive Lending

The impact of adopting AI in lending extends beyond the bank’s balance sheet. It touches the broader economy.

Fueling the “Missing Middle”

SMEs are the “missing middle” of the African economy. They are too big for microfinance but too small for corporate banking. By using financial inclusion technology to serve this segment, lenders unlock massive growth potential.

SMEs that access credit grow faster. They hire more employees and purchase more inventory. This creates a multiplier effect in the economy. For the lender, a growing SME becomes a loyal, long-term corporate client. The small trader borrowing N100,000 today could be the corporate client borrowing N100 million in five years.

Lowering the Cost of Credit

Currently, interest rates for SMEs are prohibitively high because banks must price in the high cost of manual underwriting and the high risk of default.

AI drives down both costs. Operational costs drop because automated underwriting costs cents rather than dollars. Risk costs drop because better scoring reduces defaults. As these costs decrease, lenders can lower interest rates while maintaining healthy margins. Lower rates make credit more accessible, increasing the Total Addressable Market (TAM) for the lender.

The Future is Algorithmic

The era of judgment-based lending for the mass market is over. It is too slow, biased, and expensive. The future is algorithmic.

For financial institutions in Nigeria and across Africa, the choice is clear. Continue competing for the same 20% of the market that has formal credit history, or use AI to unlock the other 80%.

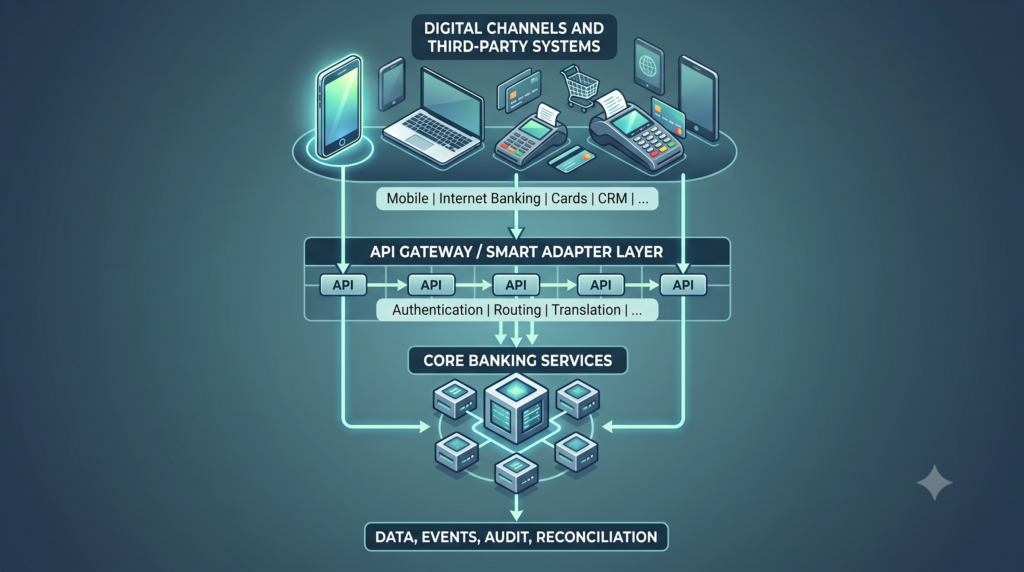

The Role of Core and Workflow Infrastructure in Safe Lending

AI models do not operate in isolation. They depend on clean data, consistent processes, and reliable execution.

This is where platforms like SeaBaas and Kusala become critical.

- SeaBaas provides the core banking foundation that captures real-time transactional data and supports flexible product configuration.

- Kusala enables automated workflows, decision routing, and auditability across the credit lifecycle.

Together, they form the operational engine that allows AI-driven lending to scale safely across different institution types and risk profiles.

Without this foundation, even the most advanced credit models struggle to deliver consistent results.

Closing the Credit Gap Without Increasing Risk

The SME credit gap in Africa is not a demand problem. It is an information problem. Traditional systems see too little of the real economy. AI changes that by turning everyday financial behaviour into actionable insight.

With credit scoring AI, lenders can expand access, improve portfolio quality, and support economic growth at the same time. The institutions that act now will define the next phase of SME lending across the continent.

The opportunity is clear. The tools exist. The question is whether lenders are ready to evolve how they assess risk.

Lend to more customers with less risk.

Modern lending requires intelligence at the core and automation across workflows. Platforms like SeaBaas and Kusala give financial institutions the foundation to deploy AI-driven credit scoring responsibly and at scale.

If you are exploring the next phase of SME lending, now is the time to build for it. Book a 30-minute clarity session to get started.

Image source: businessday.ng