Banks across Africa are under increasing pressure to move faster, operate leaner, and meet customer expectations shaped by digital-first experiences. Yet many institutions remain constrained by a legacy core banking system that was designed for a different era.

What once provided stability is now a source of friction. While fintech startups launch new features weekly, traditional banks often take months to deploy a simple update. System upgrades introduce risk. Operating costs continue to rise. Meanwhile, fintechs enter the market with flexible platforms and release new offerings in weeks, not years.

Customers do not care about backend limitations. They move to competitors who offer speed, reliability, and intuitive interfaces. For bank executives, the inability to move fast is no longer just an IT frustration. It is a strategic risk that directly impacts market share. This speed gap is rarely a talent issue. It is a structural issue.

For many banks, digital transformation is a necessity. But the real question is whether their existing core banking infrastructure is quietly holding them back.

The Hidden Cost of a Legacy Core Banking System

Legacy core banking systems are often described as battle-tested. In reality, they carry hidden costs that grow over time.

At the surface, these systems appear to function adequately. Transactions process. Accounts reconcile. Reports generate. But beneath that stability lies increasing technical debt. Each workaround, patch, and manual process adds complexity that slows the organisation down.

Common issues include:

- Heavy reliance on vendors for routine changes

- Limited internal control over configuration

- Increasing difficulty integrating new tools or channels

Over time, IT teams spend more energy maintaining systems than enabling growth. This is one of the most common yet least visible problems with old banking software.

Maintenance consumes the majority of IT budgets in traditional institutions. Banks spend significantly on patches, server maintenance, and specialists for outdated coding languages like COBOL. These operational expenses (OpEx) leave little room for innovation.

Maintaining problems with old banking software creates a cycle of technical debt. Every patch applied to a legacy system increases its complexity. Over time, the system becomes fragile. Engineers fear that changing one line of code will break a critical function elsewhere. This fear leads to extensive, expensive testing cycles for even minor changes.

Every dollar spent maintaining a legacy system is a dollar not spent on customer experience. The banking industry’s digital transformation challenges often stem from this resource drain. While fintech competitors invest in AI and user experience, legacy banks invest in keeping the servers running.

Speed to Market: Losing the Race to Agile Fintechs

Fintech competition in Nigeria is fierce. Startups identify a customer need, build a solution, and launch it within weeks. Legacy systems require complex integration and long testing cycles for new products.

Speed to market has become a defining competitive factor in banking. Customers expect new savings products, digital lending options, and personalised services. Fintechs respond quickly because their platforms are built for iteration.

Legacy systems are not.

Launching a new product often requires:

- Lengthy requirement documents

- Vendor engagement and approval

- Complex testing cycles

- Downtime windows

What should take weeks stretches into months. In some cases, banks abandon product ideas altogether because the cost and effort outweigh potential returns.

For product and digital banking teams, this creates frustration and limits experimentation. Innovation becomes incremental rather than strategic, putting banks at a disadvantage in markets where customer needs evolve rapidly.

A modern core banking system allows for configuration. Product managers can create new loan products or deposit accounts by adjusting parameters in a dashboard. A legacy core often requires hard-coding changes. This dependency on developers creates a bottleneck.

The market moves on by the time a legacy bank launches a product. First-mover advantage matters in digital finance. Being six months late with a feature often means missing the customer acquisition window entirely.

Downtime and Reliability in a 24/7 Economy

Legacy core systems were built around batch processing and end-of-day reconciliation. During these times, services go offline or slow down significantly as the system batches transactions and balances ledgers. This architecture made sense when banks closed at 4 PM. It fails in a 24/7 digital economy.

Customers transact at 2 AM. They expect instant notifications and accurate balances at all times. Downtime for maintenance or batch processing frustrates users. It signals that the bank is not a modern digital entity.

Routine upgrades often require downtime. Minor changes can trigger system instability. To compensate, teams rely on manual processes that increase the risk of error.

The consequences are significant:

- Service interruptions that frustrate customers

- Increased exposure during peak transaction periods

- Greater operational and compliance risk

From an executive perspective, system downtime is not just a technical issue. It erodes trust and exposes the institution to reputational damage.

Modern cloud-native cores offer high availability without scheduled downtime. They process transactions in real-time, eliminating the need for intrusive EOD windows. This reliability builds trust. Customers know they can access their funds whenever they need them.

High Operating Costs That Keep Rising

One of the clearest signals that a legacy core is holding a bank back is cost.

Legacy platforms often involve:

- High licensing and support fees

- Specialised skills that are scarce and expensive

- Costly integrations for even basic functionality

- Hardware and infrastructure overhead

As transaction volumes grow, these costs scale poorly. Instead of benefiting from efficiency gains, banks see operating expenses rise year after year.

These challenges limit the ability to reinvest in customer experience, analytics, or growth initiatives.

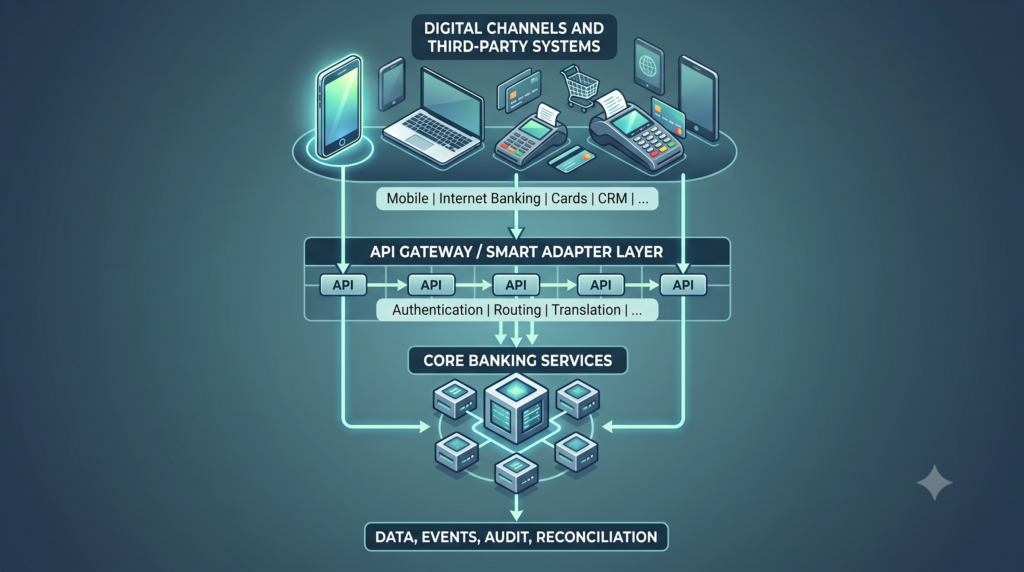

The Integration Nightmare: APIs vs. Spaghetti Code

Modern banking requires connectivity. Banks must connect to payment gateways, credit bureaus, fintech partners, and utility providers. This ecosystem approach allows banks to offer a comprehensive financial suite.

Legacy core banking systems often lack open APIs. Connecting new services requires building custom middleware. This is slow, brittle, and expensive. It creates “spaghetti code”—a tangled mess of integrations that is difficult to untangle or upgrade.

This integration barrier turns the bank into an island. It becomes unable to participate in the broader financial ecosystem. Banking system modernisation solves this by adopting an API-first architecture. This allows the bank to plug and play with third-party services, rapidly expanding its service offering without building everything from scratch.

Why Banking System Modernisation Is Now a Strategic Imperative

Modernising core banking systems is no longer an IT refresh. It is a strategic decision tied directly to growth, resilience, and competitiveness.

More importantly, modernisation gives leadership teams options. It restores flexibility and allows the institution to respond to market changes with confidence.

This is the real value of banking system modernisation. It shifts the bank from a defensive posture to a proactive one.

How to Assess If Your Bank Has Outgrown Its Legacy Core

For many institutions, the limitations of a legacy system become clear through daily experience.

Consider these questions:

- How long does it take to launch or modify a product?

- How often do system upgrades disrupt operations?

- How dependent is the bank on vendors for routine changes?

- Can the core support new digital channels without complex workarounds?

If these questions surface recurring challenges, the bank may have already outgrown its current core.

Preparing for a Transition Without Disruption

One common concern about modernisation is risk. Banks worry about downtime, customer impact, and regulatory complexity.

Modernisation does not always require a “big bang” replacement. Replacing a core banking system is a significant undertaking, but the risk of doing nothing is higher. Successful transitions follow a phased approach:

- Clear assessment of current limitations

- Gradual migration of products or services

- Parallel runs to reduce operational risk

- Selection of platforms designed for emerging markets

SeaBaas provides this agility. It offers the speed of a fintech with the robustness required for enterprise banking. It supports open APIs, real-time processing, and cloud-native scalability. This architecture allows banks to launch products fast, reduce operational costs, and deliver the reliability customers demand.

Your Legacy Core Banking System is a Competitive Liability

Legacy core banking systems are no longer neutral infrastructure. They shape how fast a bank can move, how much it costs to operate, and how effectively it can compete.

In today’s market, outdated technology creates real business risk. Banks that modernise gain agility, resilience, and the ability to define their own future.

The question facing leadership teams is no longer whether to modernise, but how long they can afford not to. Remember, the market rewards institutions that adapt. The future belongs to banks that can move as fast as their customers.

Ready to Modernize Your Infrastructure?

Stop letting your legacy core banking system dictate your business strategy. Let’s discuss how a modern core architecture transforms your speed to market.