Why Core Banking Architecture Matters More Than Ever

If you have ever waited months to launch what should have been a simple product feature because the core system is updating, you already understand the challenge many banks face today. This frustration often stems from the limitations of legacy architecture and is exactly why conversations around microservices core banking have moved from technical circles into executive discussions.

Banks rarely fail because they lack vision. They struggle because their systems cannot move as fast as their ambitions. As digital banking scales, your core banking architecture determines more than just where data sits. It dictates how quickly you can launch products, how effectively you respond to Central Bank regulations, and whether your app stays online during salary week. When a competitor launches a zero-fee transfer promo, a bank with a rigid core takes weeks to react. A bank with a modern architecture reacts in hours.

Many financial institutions still run on monolithic systems built decades ago—massive, rigid structures where changing one feature risks breaking the entire bank. Others are considering microservices core banking but struggle to separate the hype from the reality.

This choice extends beyond a technical preference for your CIO. It is a fundamental business decision. The debate between monolithic vs microservices architecture is ultimately a debate about speed, resilience, and long-term cost. One approach protects the status quo; the other builds a foundation for the future.

What Is Core Banking Architecture (Without the Jargon)?

To understand the difference, we must look at how the software is built.

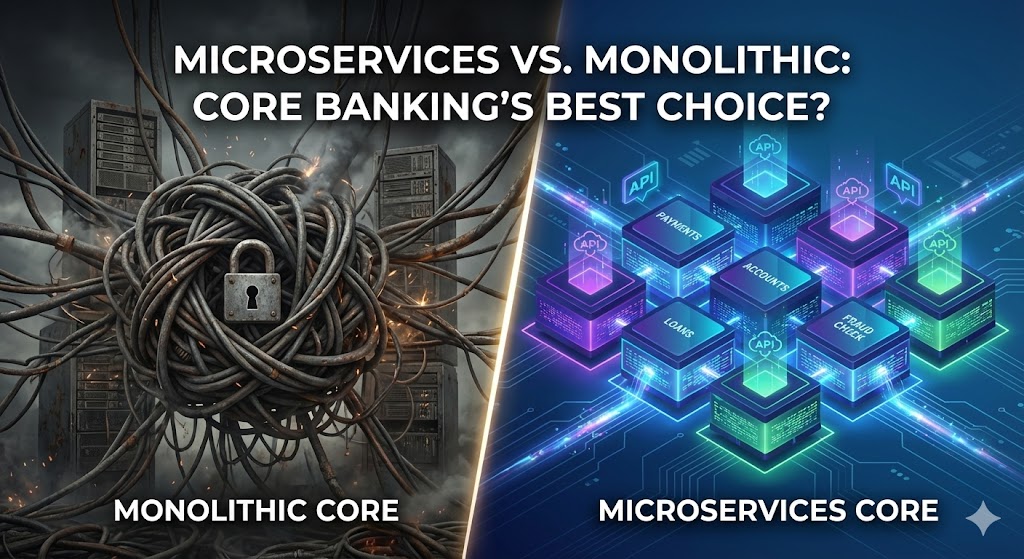

What a Monolithic Core Banking System Looks Like

Think of a monolithic system as a Jenga tower. It is constructed as one solid, interconnected block. Every function—from customer data to interest calculations—is tightly coupled within a single codebase.

This design creates a dangerous fragility. If you want to change one small piece, like adjusting a loan interest rate, you risk toppling the whole tower. Because everything is connected, IT teams live in fear of updates. A minor change requires massive regression testing to ensure it doesn’t break the entire bank.

This leads to significant operational risks. If a non-critical module like “Reporting” crashes due to a heavy query, it often drags the mission-critical “Transaction Module” down with it, taking the whole bank offline. Furthermore, scalability is wasteful. You cannot just scale the busy payment engine during salary week; you must buy more server capacity for the entire system, wasting money on resources you don’t need. This approach worked in 2005, but it fails in an era of 24/7 instant payments.

What Microservices Core Banking Means in Practice

In contrast, microservices core banking is like building with Lego blocks. The bank is constructed of hundreds of small, separate services. The “Loans” block is distinct from the “Savings” block, and they communicate via lightweight APIs.

This modern banking architecture offers distinct advantages:

- Independent Updates: You can upgrade the mobile app or launch a new savings product without touching the sensitive General Ledger. This means features launch in days, not months.

- Resilience (Fault Isolation): If the “SMS Notification Service” fails, the rest of the bank keeps running. Customers can still transfer money even if the alert is delayed.

- Cloud-Native Efficiency: You only pay to scale the parts that are busy. If 90% of your traffic is transfers, you only scale the transfer service, optimizing your cloud spend.

How Monolithic Architecture Became the Default in Banking

To understand why so many banks still operate monolithic systems today, it helps to look at the context in which those systems were created.

Why Monolithic Systems Worked in the Past

Monolithic core banking systems were a practical solution for their time. Banking products were relatively stable, with few variations and long life cycles. A savings account looked the same for years. Loan products changed infrequently. Innovation moved at a measured pace.

Transaction volumes were also far lower. Digital channels were limited, and most activity happened during business hours through branches. Systems were not expected to process millions of transactions in real time or support always-on services.

Most importantly, change was infrequent. Regulatory updates, product revisions, and system enhancements happened on predictable schedules. In that environment, a tightly coupled, all-in-one system offered reliability and simplicity. Centralised control reduced complexity, and the risk of frequent change was minimal.

Why They Struggle in Today’s Banking Environment

That context no longer exists. Modern banking operates in real time, across multiple channels, with customers expecting instant responses and continuous availability. Monolithic systems struggle to keep up because updates are slow and releases are risky. A single change can affect multiple parts of the system, increasing the chance of failure.

Scaling is also a challenge. As transaction volumes spike, monolithic systems must scale everything together, even if only one function is under pressure. This inefficiency drives up costs and limits flexibility.

This growing mismatch between system design and modern demands is at the heart of the monolithic vs microservices architecture debate shaping banking today.

The Key Differences: Monolithic vs. Microservices Architecture

To make the right choice, you need to look beyond the code and focus on capabilities. Here is how the battle of monolithic vs microservices architecture plays out on the metrics that matter most to a bank’s survival.

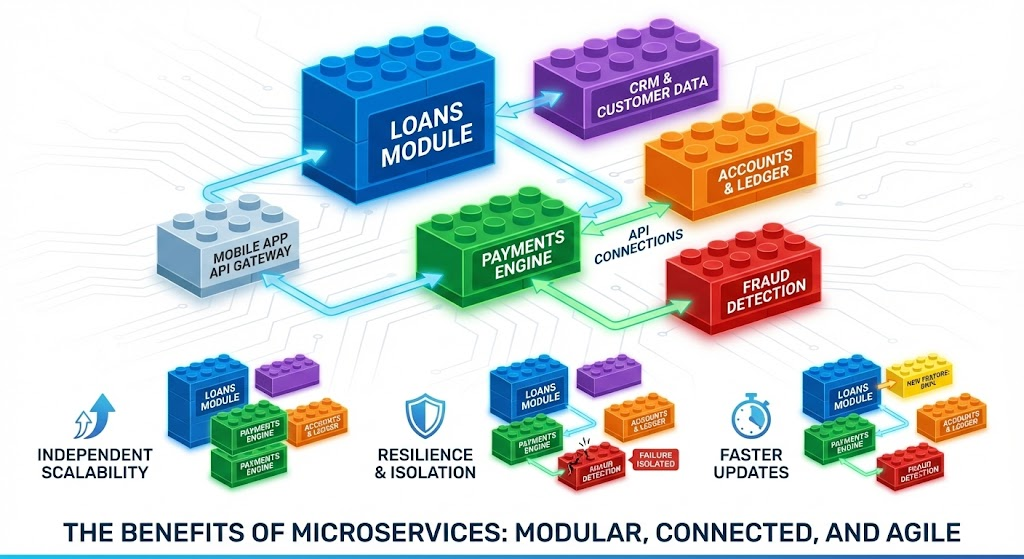

Scalability

In a monolithic system, scalability is “all or nothing.” If your payment processing volume spikes on payday, you cannot simply add more power to the payment engine. You must upgrade the server capacity for the entire bank, wasting resources on modules that are sitting idle. In contrast, microservices allow for targeted scaling. You can spin up ten extra instances of the “Transfer Service” to handle the load while leaving the “Loan Origination” service untouched. This is the definition of efficiency.

Resilience and System Stability

Monoliths suffer from the “Domino Effect.” Because the code is tightly coupled, a memory leak in a non-critical reporting module can crash the entire core, taking the bank offline. Microservices are designed for fault isolation. If the “SMS Notification” service fails, it is contained. The rest of the bank—transfers, withdrawals, and login—continues to function seamlessly.

Speed of Change and Innovation

Monoliths dictate a slow pace. Because the risk of breaking the system is so high, banks are forced into long, quarterly release cycles with heavy regression testing. Microservices unlock agility. Developers can update a specific product feature and deploy it in days, supporting a modern banking architecture that moves as fast as customer demand.

Integration with Modern Banking Tools

Finally, integration distinguishes the past from the future. In monoliths, APIs are often an afterthought—clunky “bolt-ons” that are difficult to maintain. Microservices are API-first by design. They are built to connect natively with fintech partners, payment gateways, and credit bureaus, making them the superior foundation for open banking.

Why Microservices Are Better Suited for Modern Banking

The shift to a microservices architecture is not just an IT upgrade; it is a strategic necessity. In a market where customer loyalty is won or lost on app performance, the benefits of microservices for banks translate directly to the bottom line.

Faster Product Launches

In a traditional bank, launching a new product—like a high-yield savings account for students—can take months. Developers must navigate the complexities of the entire core system, running exhaustive regression tests to ensure the new product doesn’t break existing ones. With microservices, this friction disappears. The “Student Savings” product is built as an independent service. It can be developed, tested, and deployed in weeks without ever touching the sensitive code of the main General Ledger. This allows banks to iterate at the speed of fintechs.

Continuous Improvement Without Downtime

We have all seen the dreaded “System Maintenance: Banking Services Unavailable from 12 AM to 4 AM” message. In a 24/7 economy, this is unacceptable. Microservices enable continuous improvement without downtime. Because services are decoupled, IT teams can update a specific module—say, the bill payment interface—while the rest of the bank remains live. You can fix bugs and release features in the middle of the business day with zero disruption to customers.

Easier Regulatory Adaptation

Finally, agility is compliance. When the Central Bank of Nigeria (CBN) issues a new directive on transaction limits or KYC tiers, a monolithic bank faces a major change request. A bank running on microservices simply updates the specific “Compliance” or “Limit Management” service. The change is isolated, tested, and deployed instantly, turning regulatory adaptation from a crisis into a routine configuration.

Microservices and Cloud-Native Core Banking

Microservices deliver their full value when paired with a cloud-native foundation. Together, they form the backbone of modern, scalable banking platforms.

Why Microservices and Cloud-Native Go Together

Understanding this architecture requires breaking down three key concepts:

- Containerisation (The Shipping Box): Imagine shipping goods. Instead of throwing loose items into a truck, you pack them into standard shipping containers. In software, “containers” package a microservice (like your “Transfer Service”) with everything it needs to run. This means the code works exactly the same on a developer’s laptop as it does in the bank’s production environment, eliminating the “it worked on my machine” excuse.

- Orchestration (The Traffic Controller): When you have hundreds of these containers, you need a system to manage them. Tools like Kubernetes act as a traffic controller. If a container crashes, the orchestrator instantly replaces it. If traffic spikes, it deploys more containers. It automates the health of your bank.

- Elasticity (The Rubber Band): This is the ability to stretch. In a traditional data center, you buy servers for your busiest day (e.g., Black Friday) and let them sit idle the rest of the year. In a cloud-native environment, resources expand automatically when demand is high and shrink back when it is low. You stop paying for idle capacity.

Supporting Real-Time Banking at Scale

This architecture is the only way to handle modern banking volumes. Consider the end-of-month salary rush. In a legacy bank, the transaction server gets overwhelmed, leading to failed transfers and angry tweets.

In a cloud-native microservices environment, the system detects the spike in traffic. The orchestrator automatically spins up 50 new instances of the “Transaction Service” to handle the load. Once the rush subsides, it shuts them down to save costs. This dynamic scaling ensures 99.99% uptime and zero-lag processing, regardless of volume.

Common Myths About Microservices in Core Banking

To make an informed architectural choice, we must first dismantle the myths that keep banks tethered to legacy systems.

“Microservices Are Only for Big Tech Companies”

There is a prevailing belief that microservices are the exclusive domain of Netflix, Uber, or Tier-1 global banks. This is false. In reality, smaller institutions often benefit more from this architecture. A regional bank or a specialized lender needs agility to compete with larger players. Microservices allow smaller teams to punch above their weight, deploying features and integrations that would otherwise require an army of developers on a monolithic system. It is not about the size of the bank; it is about the speed of the market.

“Microservices Are Too Complex”

Critics often point to the “distributed” nature of microservices as a source of chaos. While it is true that managing hundreds of services requires discipline, monolithic complexity is far worse—it is just hidden. In a monolith, dependencies are invisible, creating a “black box” where one change has unforeseen consequences. Microservices make these connections explicit and manageable through APIs. With modern orchestration tools, this complexity is automated, turning a tangled mess into an organized map.

“Monoliths Are Safer for Banks”

The most dangerous myth is that rigidity equals safety. Traditionalists argue that a single, solid codebase is easier to secure and maintain. The opposite is true in a digital world. A monolith has a single point of failure; if the core logic crashes, the entire bank goes dark. Microservices offer fault isolation. If one service is compromised or fails, the system automatically routes around it, keeping the rest of the bank—and your reputation—secure.

What to Look for in a Microservices-Based Core Banking Platform

Not every system labeled “microservices” is built the same. As you evaluate vendors, you must distinguish between true modern architecture and re-branded legacy code. Here is your checklist for due diligence.

True Service Independence

The most common trap in modernization is the “Distributed Monolith.” This happens when a vendor splits their application into separate services but keeps them all tied to a single, shared database. If the “Customer Service” and “Account Service” both read from the same table, you have not achieved decoupling; you have just made your monolith harder to manage. True microservices have their own private data stores. If one service fails or needs a schema update, it touches absolutely nothing else.

Strong API and Event Architecture

In an open banking ecosystem, your core must be an active participant, not a quiet vault. Look for an event-driven architecture. This means the system doesn’t just store data; it broadcasts events. When a customer makes a payment, the core should instantly publish a “PaymentCompleted” event that triggers the SMS notification, updates the loyalty points engine, and alerts the fraud detection system—all simultaneously. If the platform relies on batch jobs or polling to move data, it is already obsolete.

Observability, Security, and Governance

With hundreds of services running, you cannot rely on manual log checking. A robust platform must have native observability. This includes distributed tracing (to follow a transaction through every hop), centralized logging, and real-time metrics dashboards. Security must also be decentralized. Look for “Zero Trust” principles where every service authenticates every request, ensuring that a breach in one area cannot laterally move to sensitive core ledgers.

SeaBaas as an Example of Microservices Core Banking

Moving from theory to practice is where architectural decisions start to matter. SeaBaas provides a clear example of how microservices core banking works when it is designed intentionally, not retrofitted onto legacy systems. It is built as a system that reflects how modern banks operate today and how they need to evolve tomorrow.

Built as a Microservices-First Platform

SeaBaas is designed around modular services, each responsible for a specific banking function. This microservices-first approach allows services to operate independently while communicating seamlessly through APIs. Because APIs are foundational, not add-ons, integration with fintech partners, credit bureaus, payment gateways, and third-party services happens naturally. This also means banks using SeaBaas are prepared for open banking environments by default, without extensive re-engineering.

Designed for Banking Scale and Reliability

Resilience is engineered into the code. Leveraging a cloud-native core banking design, SeaBaas handles high transaction volumes without buckling. During peak periods like salary week or Black Friday, the system automatically scales critical services while isolating faults. If a peripheral service encounters an issue, it does not cascade to the core ledger, ensuring that your customers can always transact.

Supporting Faster Change Without Disruption

Agility is where microservices deliver their strongest advantage. SeaBaas allows banks to compose new products quickly by configuring existing services rather than requesting vendor-led changes. Launching a new student savings account or adjusting product features does not require long change requests or system-wide upgrades. Updates are safer, faster, and less disruptive, allowing banks to innovate without operational risk.

Which Architecture Is Right for Your Bank?

Choosing between monolithic vs microservices architecture is not just about following trends; it is about aligning technology with your business strategy. While a monolith might suffice for a small, localized institution with static products, most modern banks eventually face a tipping point where the old ways stop working.

When a Monolithic System Becomes a Constraint

You know your legacy core has become a liability when:

- Time-to-Market Lag: It takes months to launch a simple product, like a new savings tier, because you are waiting for a vendor patch.

- Fear of Deployment: Your IT team dreads updates because “fixing one thing breaks two others,” leading to a culture of stagnation.

- Cost Spiral: You spend more of your budget on maintaining the status quo and paying for server capacity you don’t use than on actual innovation.

When Microservices Become a Strategic Advantage

Conversely, moving to a modern banking architecture becomes a strategic necessity when:

- Digital-First Growth: Your strategy relies on high-volume mobile transactions and 24/7 availability, where downtime is a reputation killer.

- Ecosystem Integration: You need to plug into fintechs, payment gateways, and credit bureaus instantly via APIs, rather than building custom bridges.

- Scalability Demands: You experience massive traffic spikes (e.g., salary week) that crash rigid servers, requiring the elastic scaling that only cloud-native systems provide.

Conclusion: Architecture Is a Long-Term Decision

In the final analysis, the choice between monolithic vs microservices architecture is not merely a technical preference; it is a fundamental business strategy that defines your institution’s future.

Monolithic systems were designed for a bygone era of stability. While they offer centralization, they prioritize rigidity over progress, acting as anchors that limit your ability to change. In a digital-first economy, this stability has become stagnation. In contrast, microservices core banking offers a different path. It prioritizes adaptability without sacrificing control, giving you the resilience to withstand market shocks and the agility to seize new opportunities.

To build a bank that lasts, you must invest in infrastructure that supports long-term competitiveness. Your core system should be an engine for innovation, not a bottleneck.

The market moves too fast for monolithic concrete blocks. To compete, you need a system that moves as fast as your strategy.

Ready to break free from legacy limitations?

Book a Clarity Session with Peerless – Assess whether your current system is holding you back and explore how microservices-based platforms like SeaBaas support modern banking at scale.