Beyond the mobile apps, here are 10 trends in mobile banking shaping the future of Africa, which should guide what your bank or fintech must prepare for.

Mobile banking is no longer just a convenient alternative to visiting a branch; it’s the very heartbeat of finance across Africa. By 2025, a smartphone will not just be a communication device – it’s a marketplace

and a gateway to the global economy. Customers today demand financial services that are instant, intuitive, and woven into the fabric of their daily lives. For any financial institution, from a Tier-1 bank in Lagos to a microfinance institution in rural Kenya, adopting a “mobile-first” strategy isn’t just about growth anymore, survival is the game.

The statistics paint a staggering picture. The GSMA reports that Sub-Saharan Africa is the epicenter of mobile money, accounting for the majority of global transaction values. In Nigeria alone, the value of mobile transactions is soaring, driven by a young, tech-savvy population. With over 187 million mobile connections and 65% of its citizens under 35, the demand for digital-first banking is exploding. 🚀

But the mobile banking of today looks vastly different from its early days. We’ve moved beyond simple balance checks and transfers. The modern financial landscape is being redefined by powerful forces like API-first platforms, artificial intelligence, and progressive regulations.

10 trends in mobile banking to keep an eye on.

This article explores the ten key trends shaping this new era and what your institution must do to lead the charge; whether you are a universal bank that is modernizing, a neobank that is scaling, or a microfinance institution going digital.

1. Hyper-Personalization Driven by AI and Data

In 2025, generic banking is dead. True personalization goes far beyond sending a “Happy Birthday” message. It’s about creating real-time, AI-driven experiences that anticipate and respond to a customer’s unique financial journey.

Imagine your banking app noticing you’ve been spending more on fuel and proactively suggesting a budget or a cashback card for fuel purchases. This is the power of AI in action. Financial institutions are now deploying machine learning models to predict when a customer might need a loan, recommend a personalized savings plan, or flag unusual spending before it becomes a problem.

Why this matters: When customers feel understood, they stay loyal. Institutions that master personalization see higher engagement, stronger cross-selling opportunities, and significantly reduced customer churn.

2. Embedded Finance: Banking Where Your Customers Are

The most powerful trend of 2025 is that banking is escaping the confines of the banking app. Financial services are now embedded directly into the platforms people use every day, making them frictionless and context-aware.

Think about it:

- Ride-hailing & E-commerce: Super Apps like OPay in Nigeria or M-Pesa’s app in Kenya have integrated payment wallets, lending, and bill payments directly into their ecosystems.

- Retailers: When you shop online on Jumia and see a “Buy Now, Pay Later” (BNPL) option at checkout, that’s embedded finance.

- Telecommunications: Companies like Safaricom (M-Pesa) and MTN (MoMo) have become financial powerhouses by offering savings, loans, and payment services to their massive subscriber bases.

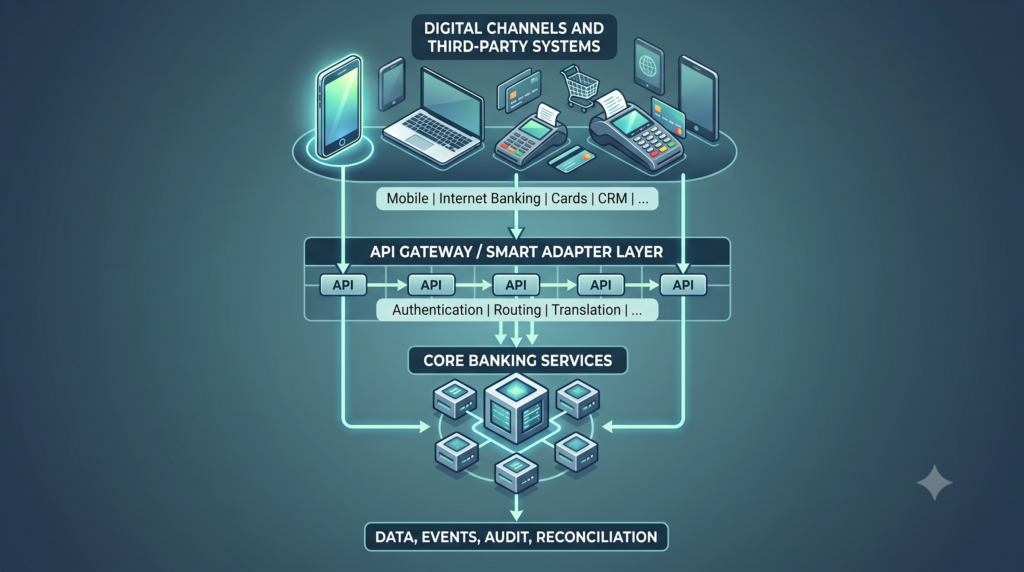

This revolution is powered by API-first core banking platforms like SeaBaas, which act as a bridge. They provide the secure, regulated “plumbing” that allows non-financial companies to seamlessly offer banking products.

Why this matters: If your bank isn’t present at your customer’s point of need, you risk becoming invisible. By embedding services, banks stay relevant, while fintechs and other businesses build powerful ecosystems and capture immense customer loyalty.

3. Regulatory Tech (RegTech) is No Longer Optional

As the digital finance ecosystem grows, so does regulatory scrutiny. Central banks across the continent, from the Central Bank of Nigeria (CBN) to the Bank of Ghana, are tightening rules around Know Your Customer (KYC), Anti-Money Laundering (AML), and data privacy. Nigeria’s Open Banking framework, for instance, is mandating new standards for secure data sharing.

Navigating this complex landscape manually is slow, expensive, and risky. This is where RegTech becomes a crucial ally. Modern banking platforms come with compliance built-in, offering automated audit trails and CBN-aligned reporting. Furthermore, workflow automation tools like Kusala help institutions streamline compliance processes, reducing bottlenecks and ensuring that everything from account opening to loan approvals is fully compliant without human error.

Why this matters: In 2025, efficient compliance is a competitive advantage. Institutions that automate and streamline their regulatory processes can scale faster, reduce operational costs, and build deeper trust with both customers and regulator

4. Financial Inclusion: Reaching the Next 100 Million

Despite incredible progress, a significant portion of Africa’s population remains unbanked or underbanked. Mobile technology remains the single most powerful tool for closing this gap. The future of growth lies not just in the urban centers but in reaching the underserved.

We see this happening in several ways:

- Digital Microfinance: Institutions like Kolomoni MFB in Nigeria are leveraging digital cores to offer loans, savings, and other services to millions of customers without the overhead of physical branches.

- USSD and Agent Banking: While smartphones are prevalent, feature phones are still widely used. Robust USSD services (like the popular *919#) and a strong agent banking network are critical for bridging the urban-rural divide and serving customers with limited literacy or internet access.

- Shariah-Compliant Fintech: For faith-driven consumers, specialized platforms like Mizan are enabling Islamic banks to offer fully compliant digital products, ensuring that financial services are accessible to all.

Why this matters: Financial inclusion is a massive business opportunity disguised as a social mission. The next wave of African banking customers will be onboarded via mobile, and the institutions that cater to their specific needs will win the future.

5. Cloud-Native Core Banking: The New Standard for Agility

LeThe rigid, outdated legacy systems that power many traditional banks simply can’t keep up with the pace of digital innovation. They are expensive to maintain and slow to change. Today, cloud-native, API-first platforms are the undisputed standard for any financial institution that wants to be agile and competitive.

Think of it like this: a legacy system is like a building made of concrete; solid, but impossible to modify. A cloud-native system, like SeaBaas, is like a structure built with advanced LEGOs. It’s modular, scalable, and can be reconfigured quickly to launch new products. This approach can lower the total cost of ownership by up to 40% and allows banks to scale seamlessly from a few thousand users to millions without a complete overhaul.

Why this matters: Cloud-native architecture future-proofs your institution. It allows you to innovate at the speed of a fintech, launch new mobile-first products in months instead of years, and stay ahead of the competition.

6. Payments Innovation Continues to Drive Adoption

Payments are the gateway to broader financial engagement, and the innovation here is relentless. In 2025, staying relevant means offering a seamless and diverse payment experience.

Across Nigeria and Ghana, QR code and contactless payments are becoming common in supermarkets and local shops. Meanwhile, companies like Flutterwave and Paystack have revolutionized cross-border remittances and online payments for SMEs, making it easier than ever to participate in the digital economy. Behind the scenes, real-time settlement infrastructures like NIBSS in Nigeria ensure that these transactions happen instantly and securely.

Why this matters: Payments are the most frequent touchpoint a customer has with a financial service. Banks and fintechs must provide frictionless integration with all major payment rails to remain the primary financial partner for their customers.

7. The Rise of Green and Sustainable Banking

Sustainability is no longer a niche concern; it’s a growing demand from customers, investors, and regulators. Forward-thinking financial institutions like Sterling Bank are using their mobile platforms to champion ESG (Environmental, Social, and Governance) principles.

This can take many forms, from simple digital-first operations that reduce paper usage and the carbon footprint of physical branches, to more advanced features like:

- Carbon tracking tools that show customers the environmental impact of their spending.

- Offering green loan products for SMEs investing in renewable energy or sustainable agriculture.

Why this matters: Embedding sustainability into your mobile offering is not just good for the planet, it’s also good for business. It strengthens brand reputation, attracts a new generation of conscious consumers, and appeals to ESG-focused investors.

8. Cybersecurity and Digital Trust as a Foundation

With increased digital adoption comes the unfortunate rise of sophisticated security threats. Cybercrime is a multi-billion dollar problem for African financial institutions. In this environment, building and maintaining digital trust is paramount.

In 2025, basic password protection is not enough. The standards are:

- Biometric Authentication: Fingerprint and Face ID are now default security features.

- AI-Powered Fraud Detection: Intelligent systems that can analyze transaction patterns in real-time to stop suspicious activity before funds are lost.

- Continuous Customer Education: Using the mobile app itself to educate users on how to spot phishing scams and protect their accounts.

Security cannot be an afterthought. It must be built into the core of the platform, with robust data security and compliance features designed to protect both the customer and the institution.

9. SME Banking and the “Super App” Revolution

Small and medium-sized enterprises (SMEs) are the undisputed engine of Africa’s economies. Yet, they have historically been underserved by traditional banks. Mobile banking is changing that narrative by providing SMEs with tools that were once only available to large corporations.

The new frontier is the SME “Super App”—a single mobile platform that combines both personal and business banking. Imagine a business owner being able to send invoices, run payroll, apply for working capital, and manage customer relationships all from their banking app.

Why it matters: SMEs in Nigeria report productivity gains of up to 35% after adopting automation tools. Banks that empower SMEs with these powerful mobile-first tools will win their unwavering loyalty and unlock a massive revenue stream.

10. Collaboration Between Banks and Fintechs

The old “banks vs. fintechs” narrative is officially over. The winning formula in 2025 is strategic collaboration. It’s a symbiotic relationship where each party brings its unique strengths to the table:

- Banks provide the regulatory licenses, established trust, and large customer bases.

- Fintechs bring the agile development, innovative technology, and a laser focus on user experience.

Core platforms like SeaBaas act as the essential bridge, enabling these partnerships through open APIs. This leads to powerful combinations, such as co-branded digital banks, fintechs white-labeling a bank’s core system, and banks embedding best-in-class fintech services directly into their own apps.

What Banks and Fintechs Must Do to Stay Ahead

The message is clear: the ground has shifted. To thrive in 2025 and beyond, financial institutions must be hyper-personalized, embedded, secure, and inclusive. The challenge is to adapt or risk irrelevance, but for those ready to lead, the opportunity is immense.

- Invest in an API-first foundation: Modernize your operations with an agile core like SeaBaas.

- Automate everything you can: Eliminate manual delays in your back-office and compliance with Kusala.

- Obsess over your customer: Use a platform like Xplorer CRM to deliver personalized, data-driven experiences.

- Embrace your role in inclusion: Leverage mobile-first and ethical-based (Mizan) solutions to serve everyone.

At Peerless, we are building the foundational infrastructure for this transformation.

Ready to lead the future of mobile banking? Book a demo with us today and discover how our suite of solutions can power your institution’s success.

Image source: pexels.com