The modern borrower has zero patience. In 2026, the expectation for credit is “now.” Whether it is a small business owner needing working capital to clear goods at the port, or a salary earner facing an emergency medical bill, the speed of access is often more valuable than the interest rate itself. This “Speed to Cash” is the new competitive battleground for Nigerian banks and fintechs.

Yet, for many institutions, the reality of lending remains painfully slow. Loan officers spend hours manually verifying bank statements. Risk managers rely on static, outdated spreadsheets to make decisions. The process is prone to human error, resulting in a binary outcome that satisfies no one: either the bank takes too long and loses the customer to a nimble digital lender, or they rush the decision and incur a high Non-Performing Loan (NPL) ratio.

Manual underwriting and rigid legacy infrastructure are the invisible brakes on your growth. They force you to choose between speed and safety.

The only way to break this trade-off is to fundamentally rethink the lending lifecycle. It requires adopting an AI loan management system, shifting from static, rule-based lending to dynamic, intelligent decisioning. However, AI is not a magic wand you wave over a broken process. It requires a specific technological foundation to function. This article explores how AI is reshaping the lending lifecycle in Nigeria and the modern infrastructure required to support it.

Top Trends Shaping AI in Lending for 2026

Artificial Intelligence in finance has moved beyond the hype phase of 2023. It is now operational, specific, and driving measurable revenue. For Nigerian lenders, three specific trends are defining the market in 2026.

1. Hyper-Personalized Pricing

For decades, banks have relied on flat pricing. Every customer in a certain bracket gets the same 25% interest rate, regardless of their individual risk profile. This approach is inefficient. It overcharges your safest borrowers (driving them to competitors) and undercharges your riskiest ones (eroding your margins).

AI enables Dynamic Risk-Based Pricing. Instead of broad segments, machine learning models analyze thousands of data points—from transaction velocity to repayment history on utility bills—to calculate a precise risk score for a specific individual at a specific moment. The system then generates a tailored interest rate. A customer with a history of early repayment might get 18%, while a higher-risk applicant gets 28%. This granularity allows banks to capture market share among prime borrowers while protecting margins on sub-prime loans.

2. Agentic AI in Collections

The traditional collections model is broken. It relies on call centers aggressively dialing debtors, often reading from rigid scripts that ignore the borrower’s context. It is expensive, abrasive, and often ineffective.

Agentic AI solves this. These are not simple chatbots; they are autonomous agents capable of negotiation and decision-making.

In a collections context, an AI agent can initiate contact via WhatsApp or SMS. It can analyze the customer’s cash flow to propose a realistic repayment plan. If the customer says, “I can’t pay N50,000 today, but I can pay N20,000 on Friday,” the Agentic AI can instantly assess if this offer falls within the bank’s acceptable risk parameters and approve it immediately, without needing human manager intervention. This reduces the cost of recovery and preserves the customer relationship for future business.

3. Alternative Data Scoring for the “Invisible”

Nigeria has a massive credit gap. Millions of creditworthy individuals and SMEs lack a formal credit history with the bureaus. Traditional loan management systems automatically reject these applicants.

AI changes this equation by scoring “Alternative Data.” Machine learning models can ingest unstructured data—such as airtime top-up frequency, SMS transaction alerts, and even device metadata—to build a proxy credit score. A market trader who has no corporate bank account but moves N2m monthly through mobile money agents is invisible to a traditional bank. To an AI loan management system, she is a prime borrower. This capability is the key to unlocking the massive underbanked sector in Nigeria.

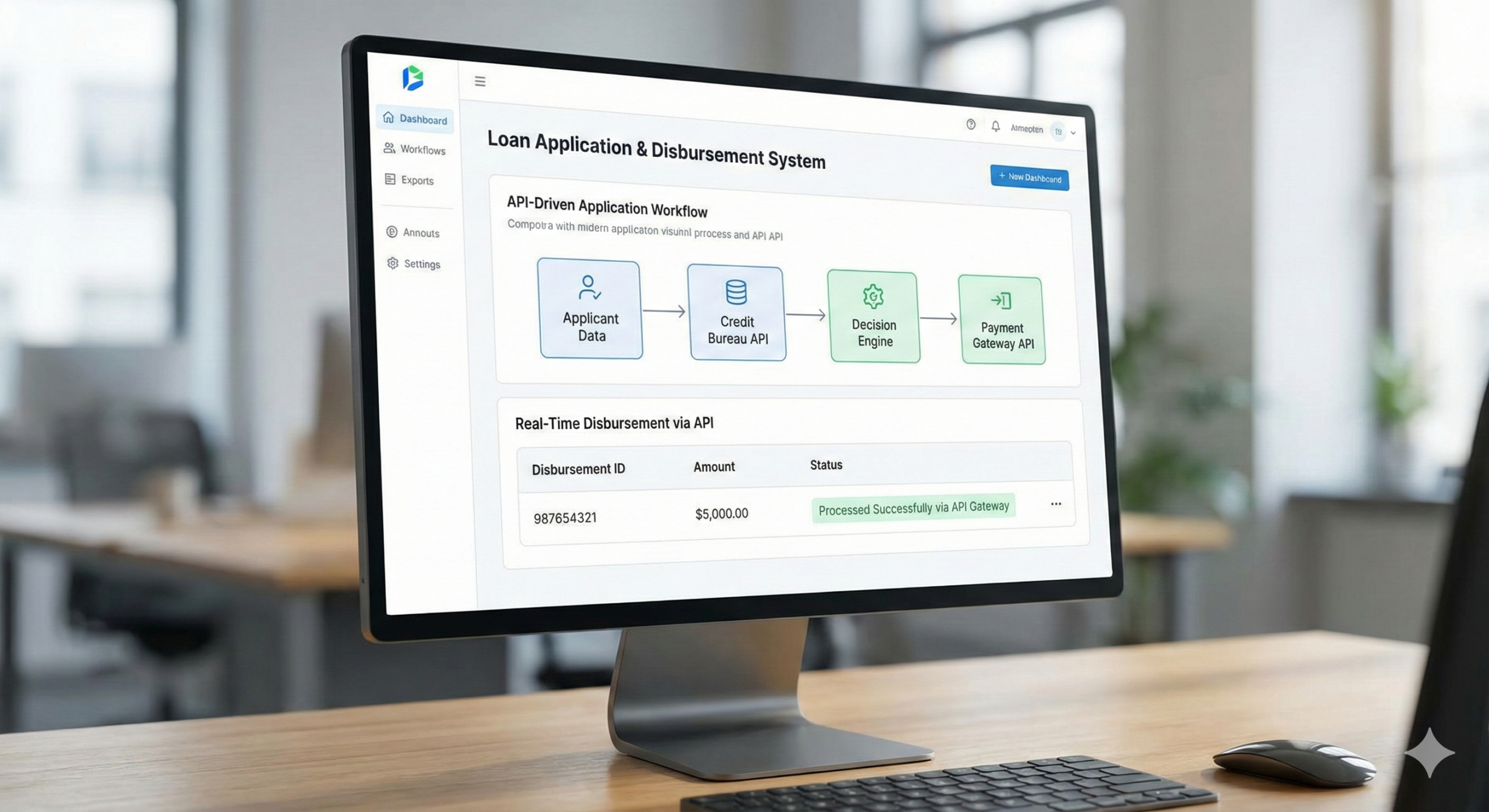

From Application to Disbursement: How AI Drives the Process

To understand the impact of AI, we must look at how it transforms the actual workflow of a loan. The goal is to move from a disjointed, manual relay race to a seamless, automated sprint.

Origination: The Zero-Touch Application

The application stage is where most drop-offs occur. Requesting customers to upload physical forms, wait for verification, and visit a branch creates friction.

In an AI-driven model, origination is Zero-Touch. When a customer uploads a bank statement or a CAC document, AI-driven Optical Character Recognition (OCR) instantly extracts the data. It does not just read the text; it understands the context. It identifies salary inflows, filters out gambling transactions, and flags inconsistencies between the stated income and the actual flows. This happens in milliseconds. The customer does not type; they simply verify. This reduces application time from days to minutes and eliminates the manual data entry errors that plague legacy systems.

Decisioning: The Brain of the Operation

This is the core of the AI loan management system. In the past, decisioning meant a credit officer looking at a checklist. Did they meet the debt-to-income ratio? Is the BVN valid?

Today, Predictive Risk Modeling takes over. The AI model does not just look at current status; it predicts future behavior. It analyzes historical trends to answer a more complex question: “What is the probability that this customer will default in the next 90 days?”

These models learn constantly. If a specific demographic of borrowers starts defaulting at a higher rate, the model detects the pattern immediately and adjusts the scoring criteria for new applicants. It is a self-correcting system that gets smarter with every loan processed.

Disbursement: The Instant Action

The final mile is often the most frustrating. A loan is approved, but the customer waits 24 hours for settlement.

In a modern setup, the decision triggers the action directly. Once the AI model approves the loan and the customer accepts the terms, the system triggers the Disbursement API. Funds are pushed instantly to the customer’s wallet or bank account. There is no manual “maker-checker” step for standard approvals. The system validates the account name, ensures the limit is available, and executes the transfer. For the customer, the experience is magical: they apply, they are approved, and they are funded, all in one session.

The Bottleneck: Why Legacy Cores Cannot Handle AI

If the technology exists, why isn’t every Nigerian bank doing this? The problem is rarely the AI itself. The problem is the foundation.

You cannot run a Ferrari engine in a bicycle. Similarly, you cannot run a real-time AI loan management system on a legacy core banking platform designed 20 years ago.

The “Garbage In, Garbage Out” Problem

AI is hungry. It needs data to function; clean, structured, and real-time data. Legacy architectures often trap data in silos. Your customer’s savings data sits in one server, their loan history in another, and their card transaction data in a third. These systems do not talk to each other.

When you try to layer AI on top of this, the model gets an incomplete picture. It might reject a good customer because it cannot see their substantial savings balance in a different module. Without a unified view of the customer, the AI cannot make accurate predictions.

The Latency Barrier

AI requires real-time interaction. When a customer clicks “Apply,” the model needs to pull data, score it, and return a decision in under two seconds.

Legacy cores operate on Batch Processing. They are designed to process transactions in bulk at the end of the day. They struggle with the high-frequency read/write requests that AI demands. If your core banking system takes 10 seconds to respond to a data query, your sleek AI lending app will time out. The user experience collapses.

API Limitations

Modern lending is an ecosystem play. You need to connect to credit bureaus, identity verification services (NIN/BVN), and open banking platforms. Legacy systems were built in an era of closed walls. Integrating them with external third-party APIs is a complex, expensive, and fragile process. Every new connection requires custom middleware and months of development. This slows down your ability to adopt new AI tools.

The Foundation of Intelligent Lending: A Modern Core

To build an AI-driven bank, you must start with the infrastructure. The prerequisite for intelligence is a Cloud-Native, API-First Core.

This modern architecture creates a Data Fabric—a unified layer where all customer data resides. In this environment, the loan management system is not a separate island; it is deeply integrated with the core. The AI has unrestricted, real-time access to the customer’s entire financial life.

This turns your core banking system from a passive ledger (which just records what happened) into an active intelligence engine (which predicts what will happen).

Accelerating AI Adoption with SeaBaas

This is where SeaBaas becomes the critical enabler for Nigerian financial institutions.

At Peerless, we recognized that banks do not just need software; they need an engine capable of powering the next decade of innovation. SeaBaas is built specifically to support the high-velocity, data-intensive demands of AI lending.

1. API-Ready Architecture for Plug-and-Play AI

SeaBaas is API-first by design. We understand that no single vendor builds the entire AI stack. You might want to use a specific credit scoring engine, a specialized OCR tool for document verification, and a distinct identity verification partner.

SeaBaas acts as the central hub. Our robust API documentation allows you to plug these AI components directly into your core workflow. You can integrate a new credit scoring model in days, not months. This gives you the agility to swap out AI vendors as the technology evolves, ensuring you always have the best-in-class tools.

2. Real-Time Data Streams

SeaBaas eliminates the latency barrier. Our cloud-native architecture supports high-frequency transaction processing.

When your AI model requests data to score a customer, SeaBaas delivers it instantly. We provide the real-time data pipelines necessary to feed your predictive models. This ensures that your decisioning is not just accurate, but instant.

3. Scalability for the “Heavy Weeks”

AI lending can create massive spikes in volume. If you launch a successful automated loan product, you might go from processing 100 applications a day to 10,000. A legacy system would crash under this load.

SeaBaas scales automatically. Our infrastructure detects the increased load and allocates the necessary computing power to handle it. You can scale your lending book aggressively without worrying that your core system will buckle under the pressure.

Conclusion

The evolution of lending in Nigeria is moving in one direction: faster, smarter, and more personalized. AI is the vehicle that gets us there, but your core banking platform is the road it drives on.

If your road is full of potholes like legacy silos, batch processing, and closed APIs, even the best AI vehicle will fail to perform. To win in the 2026 lending market, you must fix the infrastructure first. The winners will be those who can approve the fastest, price the smartest, and scale the hardest.

You do not have to rebuild this foundation from scratch. SeaBaas provides the modern, intelligent core you need to deploy AI lending today.

Ready to build a lending system that thinks? Book a Clarity Session with our experts to see how SeaBaas can power your AI ambitions and transform your credit operations.