In recent years, Africa has leapfrogged traditional banking through mobile and digital services. By 2023, there were over 330 million active mobile-money accounts in Sub-Saharan Africa. This explosive growth means millions of previously “unbanked” Africans can now send and receive money, pay bills, and access savings via their phones instead of cash. As Vice-Chair of the Association of African Central Banks (AACB) African Inter-Regional Payments Integration Task Force, Tim Masela notes, “Technology gives us an opportunity to broaden the use of financial services, including payments, savings, lending, and insurance.”

In this environment, microfinance institutions (MFIs), credit unions, and Savings and Credit Cooperative Organization (SACCOs) are upgrading their systems to reach customers. Modern core banking platforms (cloud-based, modular software engines) are at the heart of this shift. They allow MFIs to automate operations and plug into the mobile ecosystem. Microfinance providers are already seeing benefits from digitization. For clients, new channels mean convenience and security: borrowers and savers enjoy faster transactions and instant digital receipts. The gains are equally significant for institutions: automation and data cut costs and errors, while new digital products expand the customer base.

For example, a World Bank/AFI report explains that digitizing products gives clients/customers convenience and faster service, while MFIs achieve “increased operational efficiency, diversification of customer base with value-added products, and rural outreach at a lower cost”. Put simply, going digital lets microfinance serve more people for less money.

- For clients: Digital channels give faster, safer service. Customers can apply for loans or make repayments via mobile apps or USSD codes from home.

- For providers: Core banking automates back-end tasks, reducing manual labor and shrinkage. It also enables MFIs to offer savings, insurance, or value-added loans in remote areas

- For inclusion: Africa now leads the world in mobile banking, helping millions gain access where bank branches can’t reach. This creates a larger market for microfinance providers.

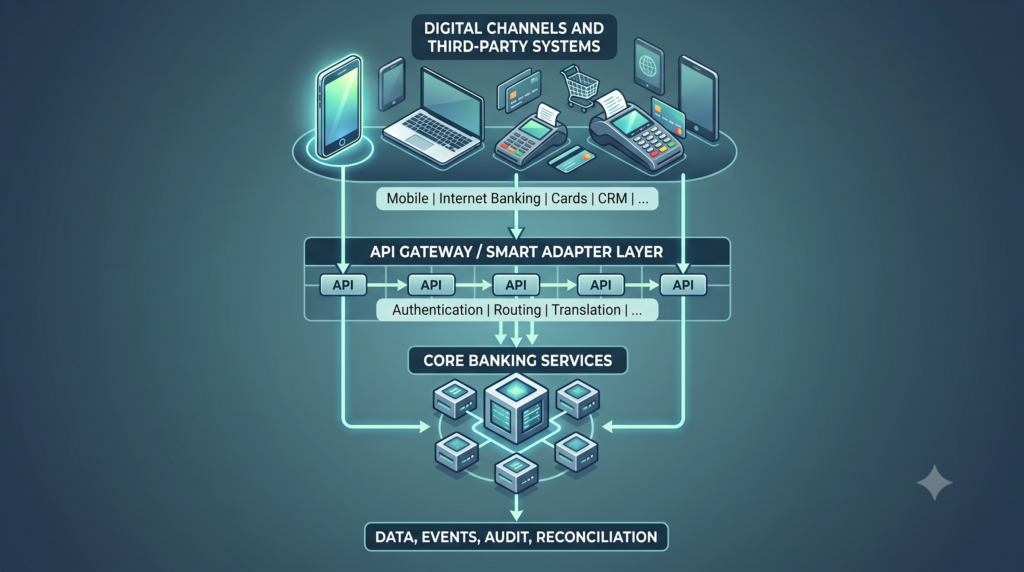

Core Banking Systems: The Engine of Modern Microfinance

A core banking system is essentially the digital engine for any lender. It manages accounts, deposits, loans, payments, and ledgers in real-time. Gone are paper ledgers and batch processing because every change made to a client’s account is immediately updated. A modern core banking platform centralizes all data and services: deposits, withdrawals, loan disbursements, savings accounts, and more. Importantly, these systems operate 24/7 and integrate multiple channels.

For example, an African-tailored core system offers real-time data and uninterrupted service across mobile, web, and agent outlets. This means an MFI in a village can update a client’s account the instant they repay via mobile money. The branch manager in the city sees it immediately.

Key features of these modern cores include:

- Real-time, always-on processing: No more end-of-day updates. The system runs round-the-clock so accounts are always current.

- Multi-channel access: Clients can use a banking app, dial a USSD code, or visit an agent kiosk which are all linked to the same core.

- Centralized data: All customer information and transactions are stored in one place, simplifying reporting and audits.

- Open APIs: The core can connect easily to mobile money networks, payment switches, credit bureaus, or fintech services via APIs.

Together, these capabilities allow even small MFIs to behave like modern banks. For example, an MFI can instantly see a customer’s balance, loan status, and payment history on one dashboard. New products (like digital micro-insurance or automatic savings plans) can be rolled out by adding modules rather than coding from scratch. In practice, this means microfinance institutions can focus on serving clients instead of spreadsheets.

Benefits of Core Banking for Microfinance

When an MFI adopts a modern core banking system, the impact on operations is enormous. Workflows that were once manual such as loan record entry, savings account reconciliation, or interest calculation will become automated. This greatly speeds up loan approvals and reduces mistakes. For example, in Nigeria Sterling Bank’s current core (SeaBaas, built with Peerless) cut transaction processing time by 60% and saved $10 million in one year. MFIs may not be this large, but even credit unions can see similar gains: faster service means higher customer trust and more repeat business.

On the customer side, members benefit from faster, more convenient service. Instead of traveling to a branch to deposit loan payments or withdraw savings, clients can use mobile money or an app. In remote areas, field officers equipped with tablets can update accounts on the spot. As one industry blog notes, mobile phone penetration is enabling MFIs to replace outdated manual processes and serve clients without building new branches. Many MFIs now allow clients to pay installments by sending money to the institution’s wallet which is not just a lifesaver in rural settings but a game-changer in the nearest future.

Modern cores also unlock new products for microfinance. Digital loan applications, automated savings programs, and even micro-insurance can be offered through the same platform. Built-in analytics and machine learning can help underwrite loans: for instance, SeaBaas includes AI-powered modules to analyze credit risk and tailor loan terms to individual customers. Real-time data also gives managers better visibility because MFIs can now detect delinquency patterns quickly and adjust policies.

Key benefits of core banking for microfinance institutions in Africa include:

- Efficiency and cost savings: Automation is a major benefit because of the significant reduction of paperwork and staff time, lowering operating costs.

- Scalability: Cloud-based cores can grow as an institution adds branches or thousands more customers. Deploying the system to a new region might be a matter of configuration rather than a new installation. In fact, top vendors advertise “rapid deployment” to help clients enter markets faster.

- Regulatory compliance: Modern systems come with inbuilt modules for local rules (AML, KYC, tax reporting). This spares MFIs from custom-coding every country’s regulations.

- Data-driven lending: Real-time reporting and analytics engines allow MFIs to monitor risk continuously and refine products. As one report notes, financial analysis tools are increasingly part of African core banking packages.

In short, core banking turns an MFI’s data into a strategic asset. It cuts turnaround times and errors while making it easier to launch the next digital service (like mobile loans or savings plans).

Case Studies and Local Innovations

Several African institutions illustrate the core banking revolution in action. In Nigeria, Sterling Bank changed their core banking infrastructure to SeaBaas. After one year of running SeaBaas, Sterling bank reported $10 million in cost savings and over 2 billion transactions processed. SeaBaas was specifically designed for African banks and MFIs, with pre-built modules and low-code flexibility to meet local needs. These advantages let Sterling and ARM Microfinance Bank innovate rapidly.

Another example is SBS Software in South Africa. In April 2025, SBS announced that its SBP Core Amplitude (a global core banking platform) would be expanded to serve microfinance institutions. The new version supports products like microloans, mobile payments, and rural savings accounts. SBS’s General Manager Camil Bennani Smires says this expansion “will strengthen SBS’s reach among new and existing microfinance clients in 17 African countries”. In other words, SBS sees core banking as the digital backbone that can scale with MFIs across the continent, helping drive inclusion in agriculture, education, and women’s entrepreneurship.

These cases show a broader point: local and specialized solutions are emerging. Beyond banks, new “neobanks” (digital-only banks) and fintech lenders are moving into formerly underbanked markets. They typically run on modern cores with API-first designs, agility, and no legacy branches. For example, digital lenders in East Africa now offer instant microloans via apps, and much of this innovation relies on flexible core banking platforms behind the scenes.

Challenges and Considerations

Despite the promise, adopting a new core banking system can be challenging for MFIs. Many microfinance organizations face limited infrastructure: poor internet connectivity or frequent power outages can undermine cloud platforms. There is also a skills gap: staff may need training to use and maintain complex software. Foreign core banking licenses are expensive – one report found Nigerian banks spent billions of naira on foreign core upgrades in 2024. MFIs with thin margins may fear a similarly steep investment.

Moreover, the transition itself can be risky. If not well-managed, moving data to a new core can disrupt services. For instance, a Nigerian microfinance bank called OurPass ran into severe troubles (including the inability to refund deposits) and blamed technical issues in its core migration. That case highlights the need for careful planning: technical glitches or staff resistance can derail the benefits of a new system.

To meet these hurdles, many MFIs take incremental approaches. Partnerships with fintechs or core vendors are common. The AFI report notes that microfinance providers often join forces with tech specialists – combining the MFI’s local presence and trust with the fintech’s innovation and IT expertise. For example, an MFI might use a third-party cloud core provider or participate in a cooperative-owned shared banking platform. This model lets institutions access modern tech without building it.

Regulators are also adapting. They increasingly allow digital licenses for MFIs and encourage interoperability. For instance, central banks in some African countries now permit “micro-savings” accounts accessible by mobile phone. Core banking solutions that offer built-in regulatory compliance (e.g. configurable KYC rules) ease the burden on MFIs by automating reporting for each jurisdiction.

In practice, MFIs must carefully evaluate any core solution before adopting it. Industry analysts advise that institutions “match the platform to strategy” (i.e. choose a lightweight cloud core for a small SACCO or a more robust system for a larger MFI). They should ensure the system is truly modular and API-enabled, so new features or partners can be added easily. Cloud/SaaS deployments are often preferable, as they reduce upfront IT costs and simplify maintenance. Finally, MFIs should look for cores with built-in compliance and real-time analytics engines. Taken together, these considerations help avoid vendor lock-in and keep the focus on serving customers.

The Fintech Frontier and Future Trends

Looking ahead, core banking will remain central to microfinance’s growth. Fintech integration is a key trend: open APIs mean MFIs can plug into wider data networks. For example, some lenders now pull mobile phone usage or social data (with permission) to help assess loan applicants. At Peerless, new financial products can be “rolled out like software features” on its platform quickly and seamlessly in weeks. This agility is crucial as customer needs continue to evolve.

We also expect more automation and intelligence. Analytical tools and machine learning will become standard for credit scoring and fraud detection. SeaBaas already includes analytics/AI features for smarter lending and customer insights. Regulators and MFIs alike are recognizing the value of digital IDs and e-KYC to onboard clients faster. In some countries, initiatives for cross-border payments and integrated systems (as advocated by leaders like Masela) could eventually let Africans use microfinance services more seamlessly across regions.

The market growth is huge: one study projects that global microfinance lending will exceed $300 billion by 2026, much of it driven by emerging markets. Africa, with its rising mobile penetration and fintech-savvy youth, will account for a growing share. Microfinance players that leverage modern cores and digital channels will be best positioned. Already, institutions that moved first to digital models report higher loan repayment rates and expanded outreach.

Conclusion

In 2025, core banking systems are transforming microfinance in Africa. By replacing manual back-office processes with cloud-native, modular software, MFIs and SACCOs can cut costs, boost efficiency, and offer 24/7 services. This directly supports financial inclusion: more clients can save or borrow through mobile phones and agents, closing the gap for those traditional banks often miss. The evidence is clear from early adopters. For instance, SeaBaas platform – which was built in Nigeria and tailored for African needs – achieved over $10 million in savings and processed 2 billion transactions in its first year, enabling lenders to extend digital wallets and fast loans to new customers.

At Peerless, we see ourselves as a crucial part of this transformation. With our SeaBaas platform, we combine rapid deployment, pre-built modules, low-code flexibility, and regulatory alignment designed specifically for African banks and MFIs. In practice, this means institutions can launch products like loans, savings, or payments in months instead of years.

Our journey, alongside other innovators in the region, shows how local, purpose-built platforms can drive microfinance into the digital age. We believe core banking technology is a catalyst for inclusive growth. By equipping microfinance institutions with modern IT, we are helping to create a future where nobody is left behind. Small farmers or shopkeepers can save and borrow with a simple tap on their phone. In 2025 and beyond, we remain committed to powering Africa’s progress through the behind-the-scenes strength of our digital core solutions.Ready to transform your institution with SeaBaas? Book a demo today

Image source: pexels.com