Many Islamic banks still depend on core banking systems that were originally built for conventional finance, then adjusted to support Islamic products. On the surface, this can look workable. The product names may be different. The approval steps may include Sharia review. The reports may even carry the right labels.

But Islamic finance needs more than labels and workflow checks.

In Islamic banking, the system has to follow the substance of each transaction. If the bank is financing an asset, the core should know when the asset was purchased, when ownership moved, and when the customer’s obligation began. If the bank is sharing profit with depositors, the system should be able to show how the profit was earned, which pool it came from, and how each customer’s share was calculated. Penalties, profit recognition, contract mapping, and ledger postings must follow the right logic from the start.

When a core system was not designed for these realities, teams are forced to compensate with manual checks, spreadsheets, custom workarounds, and constant supervision.

This guide explains why Islamic and non-interest financial institutions need purpose-built core architecture, and what a truly Sharia-first system should look like.

What Is an Islamic Core Banking System?

An Islamic core banking system is the main platform an Islamic or non-interest financial institution uses to run its banking operations in line with approved Sharia principles.

It supports everyday activities such as customer onboarding, account management, product setup, financing, transaction processing, ledger posting, approvals, reporting, and audit review. The difference lies in how the system handles the substance of Islamic finance.

For example, when the bank offers asset-based financing, the system should help teams follow the transaction properly. It should show the asset, the purchase record, the ownership flow, the customer agreement, and the related accounting treatment. Where the bank manages investment accounts, the system should help explain how profit was earned, allocated, and reported.

This matters because Islamic banking relies heavily on traceability. Product, operations, finance, technology, and Sharia teams should not have to piece together the truth from separate spreadsheets, emails, and manual notes.

A strong Islamic core gives the institution one reliable environment for configuring products, processing transactions, enforcing controls, and producing reports that management, auditors, regulators, and Sharia reviewers can trust.

For bank leaders, the question is practical: does the system simply allow Islamic products to exist, or does it help the institution run them with clarity, control, and confidence as the business grows?

Why Modified Conventional Cores Became So Common

Many Islamic banks adopted modified conventional cores for understandable reasons.

For a long time, most banking technology was designed around conventional finance. When Islamic banking began to grow in more markets, the available systems were often the same platforms already used by mainstream banks. Vendors could add Islamic product features, adjust workflows, and create custom configurations. For institutions trying to launch quickly, that felt like a practical path.

It also helped banks avoid the pressure of replacing their full technology stack too early. A conventional core with Islamic product support allowed teams to start serving customers, test demand, and build internal capability.

In smaller portfolios, this approach may look manageable. Product teams can document the rules. Sharia reviewers can approve the structure. Operations and finance teams can handle exceptions manually.

The difficulty starts when the business grows.

More products enter the market. Transaction volumes increase. Digital channels create new posting paths. Reports become more frequent. Customer expectations rise. What once felt like a manageable workaround begins to place more pressure on the people running the system.

This is why many banks now need to rethink the foundation. Modified cores helped the industry move forward when better-fit options were limited. But the next stage of Islamic and non-interest banking requires systems that can support growth with stronger control, clearer visibility, and less dependence on manual correction.

The Fundamental Flaw: Islamic Banking Is Not a Product Layer Problem

The mistake many institutions make is treating Islamic banking as something that can sit neatly on top of a conventional core.

It sounds reasonable at first. Create a new product type. Change the naming. Add approval steps. Build a few custom fields. Ask the Sharia team to review the setup. Then allow operations to manage the rest.

But Islamic finance goes deeper than the product screen.

The system has to understand what kind of transaction the bank is entering into. It must know whether the bank is buying and selling an asset, leasing an asset, sharing profit, managing an investment pool, or collecting repayment under an approved contract. That logic should not live only in policy documents or staff training manuals. It should guide how the system behaves.

When Islamic banking is treated as a product layer issue, the real work shifts to people. Product teams must remember the correct setup. Operations teams must catch exceptions. Finance teams must correct postings. Sharia reviewers must keep asking for evidence. Technology teams must keep building patches around a system that was never designed for the job.

That creates a fragile operating model.

A stronger system does not wait for someone to notice a problem after the transaction has moved. It applies the right controls before the transaction reaches the ledger. It connects the product, contract, workflow, asset record, approval trail, and accounting treatment in one clear path.

This is the real difference between a core that has been modified for Islamic banking and one that was built for it.

For Islamic and non-interest financial institutions, the question should not be, “Can this system create an Islamic product?”

A better question to ask is, “Can this system protect the integrity of Islamic banking as we scale?”

Modified Systems Create Hidden Sharia and Operational Risks

A modified core can look stable from the outside. The bank may process transactions, produce reports, serve customers, and run daily operations. The problem is that some risks do not show up immediately. They build quietly inside product setup, ledger treatment, reporting, and manual workarounds.

Hidden Interest Logic

This is one of the biggest concerns. If a core banking system was originally built around conventional lending, it may still carry interest-based assumptions in the background. The product name may change, but the calculation logic, income recognition, or ledger structure may still follow a conventional pattern.

For an Islamic bank, this creates a serious weakness. Teams should not have to keep checking whether the system has treated a transaction correctly. The system itself should prevent interest-based treatment from entering the process.

Weak Contract Enforcement

Islamic banking products must rest on valid contracts. A product should not exist only as a label in the system. The core should know the contract behind it and apply rules based on that contract.

When a modified system allows teams to create Islamic products without strong contract mapping, the bank depends heavily on human discipline. That may work in a small environment, but it becomes risky as products, branches, customers, and channels increase.

A purpose-built core should make contract mapping part of the product creation process, not an optional compliance note.

Manual Asset-Backing Validation

In asset-based financing, the system must follow the actual transaction journey. The bank should be able to confirm the asset, supplier, purchase, ownership point, customer acceptance, and related documents.

When this process happens outside the core, teams rely on emails, uploaded files, spreadsheets, and manual approvals. That makes it harder to prove what happened, when it happened, and who approved it.

The issue is not only compliance. It also affects operations. Staff spend more time chasing evidence, reconciling documents, and explaining exceptions during audits or internal reviews.

Spreadsheet-Based Profit Calculation

Many banks underestimate the risk of spreadsheets because they feel familiar. Finance and operations teams may use them to calculate profit, distribute returns, reconcile pools, or adjust deferred profit.

But spreadsheets create weak points. A formula can break. A version can change. A file can sit with one person. A manual adjustment can happen without enough visibility. Even when teams work carefully, the process becomes harder to audit and repeat with confidence.

A core banking system should reduce this burden. If profit distribution or deferred profit calculation sits at the heart of a product, the system should calculate, record, and explain it clearly.

Poor Investment Pool Segregation

For Islamic investment accounts, pool management matters. The bank must show where funds sit, how income flows into the pool, what sharing ratio applies, and how each customer’s return was calculated.

If the system cannot manage this cleanly, the bank may struggle to explain fairness across customer groups. That can create tension with customers, auditors, and Sharia reviewers.

The stronger approach is to let the core track pool balances, weightages, utilization, profit share, and customer allocation in a way that the bank can reproduce at any time.

Incorrect Penalty Treatment

Late payment handling can become sensitive in Islamic finance. A conventional system may treat penalties as income by default, unless the bank creates a workaround.

That is a risky place to depend on manual correction.

The system should help teams apply the approved treatment from the beginning. If a penalty should not become bank income, the core should make that treatment clear in the configuration, posting, reporting, and audit trail.

Weak Auditability

Auditability is not just about having logs. The bank must be able to trace the life of a transaction from product setup to approval, execution, ledger posting, and reporting.

Modified systems often scatter this evidence across different places. The product team has one record. Operations has another. Finance keeps a reconciliation file. The Sharia team has approval notes. Technology may hold custom configuration details.

When questions arise, the bank spends too much time rebuilding the story.

A good core should make the story visible from the start.

Regulatory and Sharia Board Pressure

Islamic banks operate in a trust-heavy environment. Regulators want reliable reporting. Sharia boards want confidence that approved principles are followed in daily operations. Management wants assurance that the bank can scale without creating hidden exposure.

Modified systems make this harder because they often depend on people catching problems after the fact.

A purpose-built Islamic core reduces that pressure. It brings product rules, transaction controls, ledger safeguards, audit trails, and reporting into one operating structure. That gives leaders stronger confidence that the institution is not just offering Islamic products, but running them on infrastructure designed for the work.

Purpose-Built vs Modified Islamic Banking Software

During a demo, modified banking software and a purpose-built Islamic core may look similar. Both can show product setup, customer accounts, approvals, reports, and ledger activity.

The difference becomes clearer when the bank reviews how the system handles Islamic finance beneath the interface. A modified conventional core often depends on configuration, custom fields, extra workflows, and manual supervision. That may help the bank operate, especially at the early stage, but it can create pressure as products and transaction volumes grow.

A purpose-built Islamic core gives the bank stronger control because the structure of Islamic finance sits inside the operating model. Product setup, contract rules, asset flow, profit treatment, transaction checks, and reporting follow a more reliable path.

| Area | Modified Conventional Core | Purpose-Built Islamic Core |

|---|---|---|

| System foundation | Conventional banking logic adjusted for Islamic products | Built around Islamic finance principles |

| Product setup | May depend on custom fields and special configurations | Follows contract-based product setup |

| Contract governance | Often handled through documents or workflow notes | Built into product creation and approval |

| Asset-backed financing | Asset checks may sit outside the core | Asset flow can be tracked within the process |

| Profit calculation | May depend on spreadsheets or custom logic | Can calculate and record profit treatment clearly |

| Investment pools | May require manual reconciliation | Can support clearer pool tracking and allocation |

| Penalty handling | May need workarounds to avoid wrong treatment | Can apply approved penalty handling from setup |

| Ledger posting | Relies heavily on review and staff controls | Can enforce posting restrictions inside the system |

| Audit trail | Evidence may sit across several teams and tools | Activity can follow one traceable path |

| Scalability | Growth can increase manual checks and custom fixes | Growth can happen with stronger built-in controls |

For leaders, this comparison should lead to one practical question: will the system still protect the institution when the bank grows beyond today’s operating volume?

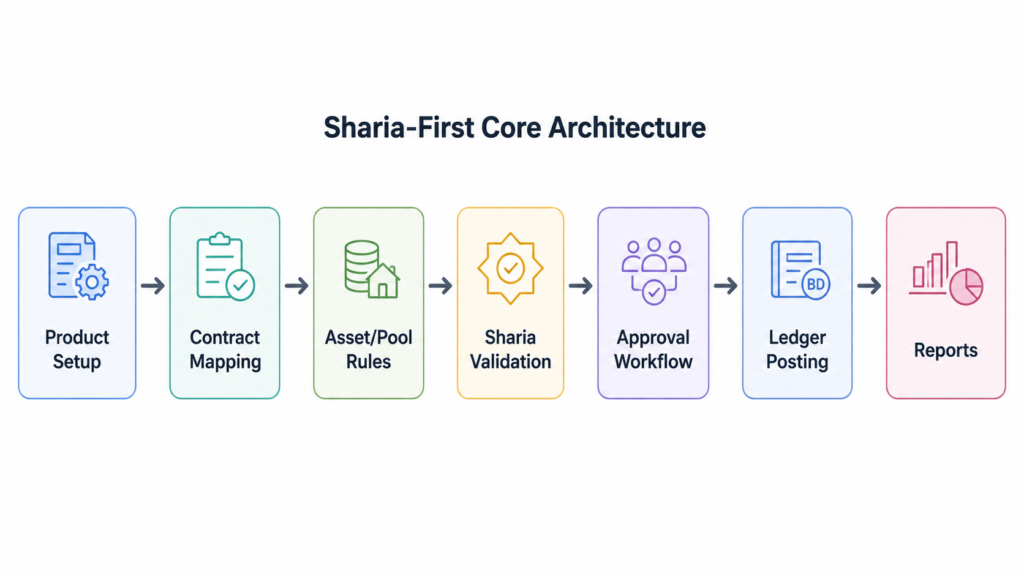

What a Truly Sharia-First Core Architecture Looks Like

A Sharia-first core is not defined by the number of Islamic products it can display on a menu. It is defined by what the system allows, prevents, records, and proves.

For Islamic and non-interest financial institutions, architecture matters because every product decision eventually becomes an operational, accounting, compliance, and customer trust issue.

Ledger-Level Removal of Interest Logic

The ledger is where the system reveals what it truly believes.

If a core still carries interest accrual logic at the base layer, the bank has to keep watching the system carefully. Product teams may configure the product properly, but the institution still has to confirm that income recognition, account treatment, and GL postings do not follow conventional lending patterns in the background.

A Sharia-first core should remove that ambiguity. The system should not treat interest as something to hide, rename, or disable through workaround settings. It should operate from a non-interest foundation, so product and finance teams do not spend their time correcting logic that should never have existed in the process.

Mandatory Contract Mapping

Islamic banking begins with the nature of the contract. The system should know whether a product is based on Murabaha, Ijara, Mudarabah, Musharakah, or another approved structure.

This should happen inside product creation, not in a separate policy note that sits outside the core.

When contract mapping becomes mandatory, the bank reduces the chance of launching products that carry the right name but lack the right structure. It also gives Sharia reviewers a clearer way to evaluate the product because they can see the contract logic tied to configuration, workflow, and ledger treatment.

Embedded Asset-Backing and Ownership Flow

For asset-based financing, documentation alone is not enough. The system should help the bank follow the transaction journey from customer request to asset purchase, ownership confirmation, sale or lease execution, and customer obligation.

This protects both compliance and operations.

If the bank cannot show when the asset entered the transaction, when ownership moved, and what evidence supports the process, teams may struggle during reviews. A Sharia-first core should make this trail visible without forcing staff to rebuild the story from emails, attachments, and spreadsheets.

Sharia Validation Before Ledger Posting

A strong Islamic core should not wait until the end of the day for someone to notice a problem. It should apply the right checks before a transaction reaches the ledger.

For example, if a Murabaha process requires asset purchase before customer sale, the system should not allow the transaction to skip that step. If a posting attempts to enter a restricted GL account, the system should reject it. If a penalty has an approved non-income treatment, the posting path should reflect that from the start.

This is where architecture becomes practical. It helps teams prevent errors instead of only detecting them later.

Pool-Based Profit Distribution

Profit distribution in Islamic banking must be clear, fair, and reproducible. The bank should be able to explain how funds entered a pool, how income was allocated, what sharing ratio applied, and how each customer’s return was calculated.

When this sits outside the core, the process can become difficult to defend. Even careful teams can run into version-control issues, manual adjustments, and reconciliation gaps.

A Sharia-first system should keep pool balances, weightages, utilization, profit share, and customer allocation within a traceable process. That gives finance, operations, and Sharia teams one version of the truth.

Product, Transaction, and GL-Level Controls

Compliance should not depend on one control point. A good system applies discipline across the product lifecycle.

At product level, the core should guide what can be created and what must be approved before launch. It should check whether the activity follows the approved contract and workflow, at transaction level. And at GL level, it should ensure that the accounting treatment does not contradict the institution’s Sharia position.

This layered control matters because errors can enter at different points. The stronger the architecture, the less the bank depends on after-the-fact correction.

Real-Time Reporting for Sharia Boards and Regulators

Sharia governance does not end with product approval. Boards, management teams, auditors, and regulators need visibility into how products behave after launch.

A Sharia-first core should support reports on product performance, asset-backing, profit distribution, exception handling, approvals, and ledger postings. The goal is not only to produce documents during review periods. The goal is to give leadership ongoing confidence that the bank’s operations match its approved principles.

API-First Integration With Ledger Protection

Islamic banks also need modern digital infrastructure. They need mobile banking, payment integrations, identity validation, customer onboarding, agency channels, analytics, and third-party connections.

But integration should not create a backdoor around compliance.

An API-first Islamic core should allow the bank to connect with external systems while still passing transactions through the right validation before ledger posting. This helps the bank innovate without weakening the controls that make Islamic banking trustworthy.

A truly Sharia-first architecture gives the bank room to grow while protecting the substance of the business. It allows leaders to move faster because the system itself carries more of the discipline.

What CIOs and CTOs Should Look For in an Islamic Core Banking System

For CIOs and CTOs, the evaluation should go deeper than product screens and feature lists.

A vendor may show Islamic product setup, approval workflows, reports, and digital integrations. Those are useful, but technical leaders need to understand how the system behaves underneath. The real test is whether the architecture can support Islamic banking operations without creating hidden control gaps.

Start with the ledger. Review how the system handles profit, penalties, receivables, investment pools, income recognition, and restricted postings. Then examine product configuration, transaction validation, reporting, audit trails, integration controls, and scalability.

The questions below can guide a practical vendor review.

| Evaluation Area | Question to Ask |

|---|---|

| Ledger design | Does the system remove or merely hide interest-based logic? |

| Product setup | Must every Islamic product follow a valid contract structure? |

| Asset flow | Can the system track asset purchase, ownership, and customer obligation? |

| Transaction control | Can non-compliant actions be blocked before ledger posting? |

| GL safeguards | Can restricted postings be rejected automatically? |

| Profit treatment | Can the system calculate and explain profit distribution clearly? |

| Auditability | Can users trace product setup, approvals, transactions, and postings? |

| Reporting | Can the bank generate Sharia, regulatory, and management reports without manual reconstruction? |

| Integration | Do API transactions still pass through the right validation controls? |

| Scalability | Can the architecture support growth without weakening governance? |

The right Islamic core should make technology leadership more confident, not more dependent on custom fixes. It should give the bank a cleaner foundation for product delivery, integration, reporting, and long-term governance.

What CEOs Should Care About: The Business Case for a Purpose-Built Islamic Core

A CEO may not need to know every configuration detail inside the core banking system. But the CEO should care deeply about what the system makes possible, what it slows down, and what risks it quietly carries.

Faster Product Launch

Islamic banks compete in markets where customers expect modern banking experiences. Waiting too long to launch a new product can mean losing deposits, financing opportunities, and customer trust.

A purpose-built Islamic core shortens the distance between product idea and market launch because teams do not have to rebuild Sharia controls each time. Product setup, contract logic, approval workflows, profit treatment, and reporting can follow a clearer path from the start.

This matters for growth. When the bank can introduce well-governed products faster, innovation becomes less dependent on custom patches and long vendor cycles.

Reduced Compliance Exposure

Compliance failures in Islamic banking affect more than operations. They can damage trust with customers, regulators, investors, and Sharia boards.

A modified core often pushes too much responsibility to manual review. People have to catch what the system does not understand. That creates risk, especially as transaction volumes grow.

A purpose-built core lowers this exposure by bringing controls closer to the transaction. It helps prevent wrong product setup, weak asset validation, incorrect profit treatment, and restricted ledger postings before they become bigger issues.

Stronger Sharia Board Confidence

Sharia boards need more than periodic explanations. They need visibility into how approved principles show up in daily banking activity.

When the system can show contract mapping, approval trails, transaction history, profit allocation, asset evidence, and ledger treatment, reviews become more grounded. The board no longer has to depend only on reconstructed reports or explanations from different teams.

That kind of visibility strengthens governance and gives leadership more confidence in the integrity of the institution.

Better Operational Efficiency

Manual work has a cost. It takes time, slows decisions, creates reconciliation pressure, and increases the chance of errors.

In many banks, operations and finance teams spend too much time checking product behaviour, adjusting reports, moving between spreadsheets, and confirming that system outputs align with approved Islamic finance rules.

A purpose-built core reduces that burden. Teams can spend more time serving customers and improving products, rather than constantly compensating for system limitations.

Digital Growth Readiness

Islamic banks cannot afford to remain digitally slow because of compliance complexity. Customers still expect mobile access, fast onboarding, smooth payments, and reliable service.

A modern Islamic core should support digital channels and third-party integrations while protecting the ledger from non-compliant activity. That balance matters. Growth should not force the bank to choose between better customer experience and stronger Sharia governance.

Market Expansion

As Islamic and non-interest financial institutions expand across markets, leadership needs a system that can support different regulatory expectations, product structures, approval requirements, and reporting formats.

A purpose-built core gives the bank a stronger foundation for expansion because the architecture already understands the core principles of the business. The institution can enter new markets with more confidence, instead of carrying old workarounds into bigger environments.

Common Islamic Banking Products a Purpose-Built Core Should Support

A purpose-built Islamic core should do more than list Islamic products on a menu. It should understand the structure behind each product and help the bank manage the full journey from setup to reporting.

Murabaha

Murabaha is commonly used for cost-plus asset financing. The bank purchases an asset and sells it to the customer at an agreed markup, with the cost and profit clearly disclosed.

Inside the core, this should not behave like a normal loan with a different name. The system should help the bank track the asset request, supplier details, purchase confirmation, sale price, customer acceptance, repayment schedule, deferred profit, and accounting treatment.

The most important control is sequence. The bank should not complete the customer sale before the asset purchase and ownership flow have been properly captured.

Ijara

Ijara is a lease-based structure. The bank or financier owns the asset and leases it to the customer for an agreed rental amount over a defined period.

A core that supports Ijara properly should track the asset throughout the lease lifecycle. This includes the asset record, rental schedule, ownership status, maintenance-related responsibilities where applicable, payment history, termination events, and any approved transfer arrangement at the end of the lease.

Without this structure, teams may end up managing asset details outside the core, which weakens visibility and makes reviews harder.

Mudarabah

Mudarabah is a profit-sharing arrangement where one party provides capital and another manages the business or investment activity. In banking, it often applies to investment accounts and profit distribution.

The core should make profit distribution clear and traceable. It should show the pool, the funds assigned to it, the agreed sharing ratio, the income allocated, and the basis for each customer’s return.

This matters because depositors and Sharia reviewers need confidence that profit was not guessed, smoothed manually, or distributed through unclear calculations.

Other Islamic Finance Contracts

A strong Islamic core should also provide room for other approved structures, depending on the institution’s product strategy and Sharia governance framework.

These may include Musharakah for partnership-based financing, Salam for advance-payment transactions, Istisna for manufacturing or construction-related financing, and Wakalah for agency-based arrangements.

Not every institution will launch all of these products at once. The important thing is that the core should give the bank a reliable foundation to configure, approve, monitor, and report each product according to its actual contract structure.

That is what separates a system that merely accommodates Islamic banking from one that can support it with real operational confidence.

The Migration Question: Moving From a Modified Core to a Purpose-Built Islamic Core

Many Islamic banks know their current core has limitations, but changing a core banking system is never a light decision. It affects operations, customers, finance, compliance, integrations, reporting, and internal routines.

That is why migration should begin with a careful review of how the bank currently runs its Islamic products.

The institution should examine existing product structures, contract templates, approval flows, customer data, financing records, chart of accounts, reports, and third-party integrations. This helps the team identify what can move cleanly, what needs correction, and what should be redesigned before go-live.

A migration project also gives the bank a chance to clean up old compromises. Some products may depend too much on manual checks. Some reports may require spreadsheet work before they become usable. Certain approval steps may sit outside the core. Ledger mappings may also need review before they enter a new system.

The best migration teams bring product, operations, finance, risk, compliance, Sharia review, and technology into the process early. Each team understands a part of the current operating reality.

A practical plan should cover system assessment, data review, product mapping, contract alignment, ledger review, integration planning, user training, testing, go-live preparation, and post-launch support.

Migration requires care, but delay also carries a cost. Leaders should ask one honest question: how much effort are we already spending to make the current system behave like an Islamic core?

The Structural Answer for Islamic and Non-Interest Financial Institutions

Islamic and non-interest financial institutions need core systems that understand how their business actually works.

This is the role Mizan was built to play.

Mizan is a purpose-built digital banking core designed for Islamic and non-interest financial institutions. Its architecture supports the realities that matter in Islamic banking, including contract discipline, non-interest ledger logic, asset-backed financing, profit distribution, approval controls, audit trails, and reporting.

For product teams, this means Islamic finance products can be configured with clearer rules from the start. Operations teams gain workflows that reduce scattered manual checks. Finance teams get stronger structure around profit treatment, penalties, pools, and postings. Sharia reviewers can follow product and transaction activity with better visibility.

Mizan also supports modern digital banking needs. Through its API-first architecture, institutions can connect to payment gateways, identity systems, mobile banking apps, card processors, fintech wallets, and other external platforms, while transactions still pass through Sharia validation before ledger posting.

The real value is confidence.

- Confidence that products follow approved contract logic.

- Confidence that transactions pass through the right checks.

- Confidence that reports can support internal review, Sharia oversight, and regulatory scrutiny.

For Islamic and non-interest financial institutions, the core banking decision shapes how the bank builds products, serves customers, satisfies regulators, and protects trust.

Mizan gives institutions a stronger foundation for that work, with architecture designed around the substance of Islamic finance.

Final Checklist: Is Your Current Core Truly Built for Islamic Banking?

Before choosing a new core or renewing confidence in your current one, use this checklist as a practical internal review tool.

| Question | What to Look For |

|---|---|

| Can every Islamic product be linked to an approved contract structure? | Product setup should connect clearly to the right Islamic finance contract. |

| Does the system track asset flow where required? | For asset-backed financing, the core should show purchase evidence, ownership flow, and customer obligation. |

| Can the system stop a transaction before it breaches approved rules? | Validation should happen before ledger posting, not only during later review. |

| Are restricted GL postings blocked by the system? | The bank should not rely only on manual checks to prevent wrong accounting treatment. |

| Can profit distribution be explained from system records? | Finance teams should not have to rebuild critical calculations on spreadsheets. |

| Does penalty treatment follow the approved structure? | The system should support clear handling without confusion around income recognition. |

| Can Sharia reviewers trace product and transaction history? | The trail should show setup, approvals, changes, transaction movement, and ledger postings. |

| Are reports generated from clean system data? | Management, auditors, regulators, and Sharia boards should not depend on heavy manual reconstruction. |

| Do third-party integrations pass through validation before posting? | Digital channels and APIs should not bypass the controls inside the core. |

| Can the platform scale without making governance harder? | More customers, products, branches, and transactions should not create more workaround layers. |

If several answers are unclear, your teams may already be carrying too much of the system’s burden.

A core banking system for Islamic finance should help the institution protect its principles through product configuration, transaction processing, recordkeeping, and reporting.

Conclusion: Islamic Banks Need Infrastructure That Thinks Like Islamic Finance

Islamic banking cannot depend forever on systems that were built for a different model of finance.

A modified core may help an institution launch products, serve customers, and run daily operations. But as the bank grows, the hidden cost becomes clearer. Teams spend more time checking exceptions, rebuilding reports, validating transactions, reviewing product behaviour, and making sure the system has not quietly applied the wrong logic.

That is not a strong foundation for scale.

Islamic and non-interest financial institutions need infrastructure that understands the substance of the business. The core should recognise contracts, asset flows, profit treatment, investment pools, approval controls, ledger rules, and reporting obligations as part of normal banking operations.

This is not about adding more complexity. It is about reducing the burden on people by giving them a system that already carries the right discipline.

At the leadership level, the stakes are clear. The CEO has to protect trust and long-term growth. Technology leaders need architecture that can scale without creating new risks. Sharia reviewers need visibility they can rely on. Operations and finance teams need fewer manual corrections and clearer system evidence.

A purpose-built Islamic core gives the institution a better way to grow. It helps the bank protect its principles while improving speed, control, and customer service.

Mizan was designed for this reality. As a purpose-built digital banking core for Islamic and non-interest financial institutions, it gives banks a stronger foundation for product innovation, daily execution, Sharia governance, and future expansion.

If your institution is reviewing its core banking infrastructure, this is the right time to ask a deeper question:

Is your system only supporting Islamic banking, or is it truly built for it?